This article seems to focus on all of the upsides of indexing, which are all true. However, those upsides don't negate the risk that is being pointed to.

* "The tail is not wagging the dog" - index funds are a relatively small percentage of total share ownership.

* "Benchmark huggers have always been around" - owning ~the index was not started with index funds.

* "Active funds literally own the market" - the sum of portfolios of non-index funds ends up having the same profile.

* "Price discovery is a cop-out" - relatively small part of the trading volume.

* "Liquidity is not a huge problem for index funds" -no market impact to sell (v dubious if you ask me), unlevered.

* "Humans matter more than fund structures" - the absence of index funds did not prevent bubbles/crashes.

You can disagree with those points (I do with some of them) but that's a large part of the article.

If you're talking about index mutual funds, then the author is just plain wrong. Any open-ended fund offering daily liquidity will trade, and therefore produce market impact, to meet its daily redemptions.

If you're only talking about ETFs, then this is technically correct. Besides the occasional index re-constitution, unlevered index ETFs don't do any trading. However it's definitely not true that there's no market impact. As the fund grows (or shrinks) the shares just don't magically appear in the portfolio. Somebody has to go out and buy (or sell) those shares, and like any trading volume, that creates market impact.

The mechanism that ETFs actually use is something called "Authorized Participants" (or APs for short). Basically market makers have the right to create or redeem shares in the ETF. To create new shares, they go out and buy all the stocks in the index, then hand a basket over to the ETF fund manager, who then hands back new shares of the equivalent value. And to destroy shares, the AP hand over shares in the ETF, and the fund manager hands back a basket of shares from the index.

If there's high demand for investors to own the ETF, that'll push up the ETF's stock price. As the price rises relative to the index value, APs will detect an arbitrage opportunity. They'll go out and buy the basket of stocks in the index at a cheaper price, then create new ETF shares at the richer price, and pocket the difference. Vice versa if there's demand from investors to exit the ETF.

The mechanism keeps the ETF price closely pegged to the index, because the further out of line it gets the more arbitrageur activity pushes it back in line. While also flexibly satisfying investors' specific demand for the ETF at any given time. Basically it delegates the role of trading from the fund manager, who usually doesn't have any special expertise in trading, to highly specialized trading firms and market makers.

However, as you can clearly see, market impact most definitely exists. If a flurry of investors rush to enter or exit an ETF, then a huge amount of trading has to be done to create or redeem the shares. Just because the APs create this trading impact, instead of the fund itself, is a distinction without a difference. The underlying stocks in the index are subject to market impact.

I think they claim is that their is a lot of "dumb money" holding indexed products that are likely to sell all at once when things turn south. By the structure of these funds, their will be large selling pressure on the underlying stocks and a good chunk of them don't have the liquidity to support that pressure. That doesn't mean their will be a metldown, just that prices will tank very hard and a lot of people will lose a lot of money + the economic effects that has I don't understand.

I was hoping the original article would tear that reasoning down, and while it did touch on various mechanisms it didn't give a cohesive thesis as to why that is wrong.

Derivatives written against sub-prime holdings tipped the balance when the fan was hit. There are tons of derivatives written against the indices, thus indirectly against those funds.

But the position is serious when enterprise becomes the bubble on a whirlpool of speculation.

When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.

(John Maynard Keynes, General Theory, Chapter 12, page 142 in the Google Book edition)

The fundamental problem he seems to be pointing at is that notional replicating portfolios can work like an engineering marvel in good times and become inoperable in bad (liquidity) times.

There were many elements to the CDO crisis -- including bad faith by the rating agencies and a prolonged asset-price mania much beyond this stock-market rally. The simpler metaphor is the emission of vanilla stock options. In principle, a bank is only able to offer options because he has the ability to replicate it and neutralize his risk. But if market conditions diverge from the asset replication model, then boom you get LTCM.

https://awealthofcommonsense.com/wp-content/uploads/2019/09/...

At least for exchange-traded funds, it would seem that you don't have to actually destroy units of the ETF in the case of a sell-off. The ETF units would just sell at lower prices, just like when there is a 'sell off' of any stock - there are always equal numbers of buyers and sellers, you don't destroy units, you just move the price lower.

With index funds where you have an account directly with vanguard or whoever instead of buying units on an exchange, I'm not sure how it works in a sell-off. Perhaps they sell shares in the individual stocks, or perhaps they just try to sell off your shares bundled together by issuing more ETF units. I don't know what they do, but it seems like there are a bunch of options that should mean they don't have to sell off illiquid stocks on command.

I'm not sure. Happy to be enlightened. As much as I think about it, my intuition seems to consistently say that it's impossible for index funds to be broken in any meaningful way that's any different from the market itself or some sector thereof being in a bubble.

First, I think he didn't made that point very clearly. Second, why would they be sold at a larger discount than larger holdings? It is all in proportion - they own less and sell less of the smaller holdings.

(There are issues conceivable where you have a liquidity mismatch (bonds, real estate), but I haven't seen a solid elaboration of that point. It's the good old "people worry about bond market liquidity" meme that Mark Levine pokes fun at in his Bloomberg Column "Money Stuff".)

I guess there are more legitimate concerns for funds that hold bonds or real estate or other less-liquid assets. But the solution to that is just, don’t put yourself in a position where you have to liquidate those funds in a crunch.

Even if one of the underlying stocks becomes illiquid, a big enough price divergence on all of the other liquid stocks would make it profitable to eat the loss or hold the illiquid ones (risky, but remember, there are many authorized participants competing with each other so if there is some way to make an easy arbitrage profit, they will find a way). You'd basically need the entire market to become illiquid.

[0]: https://www.investopedia.com/terms/a/authorizedparticipant.a...

If the index instruments have a lot more liquidity than the underlying names, then that means they won't be able to gracefully absorb the liquidity shocks from an unwind in the index.

Here's some back of the envelope calculations. Between SPY, IVV, and VOO alone, there's $500 billion in S&P 500 index ETFs. Consider if an unwind event leads to 20% of index assets being redeemed in a single day. That's $100 billion from the above ETFs alone.

Now consider a typical thinly traded single-name stock like Chubb Limited (symbol CB). CB makes up 0.3% of the S&P 500 by weight. So in the hypothetical scenario above, the APs would have to collectively sell $300 million worth of CB in a single day. Chubb's entire ADV is only $238 million.

Trying to sell more than 100% of a stock's ADV in a single day is guaranteed to produce huge market impact. The current liquidity providers in CB almost certainly cannot absorb that amount of trading volume all in one direction. In that scenario, Chubb's stock might fall by 20%, for something that had nothing to do with the company itself.

I think the overall point is that a lot of single-name stocks nowadays don't really have much of an individual market. Names like TSLA, FB or TEVA definitely have a robust market with a lot of traders still focused on company specifics. But a lot of the more boring, lower volatility, mid-cap stocks (like CB) mostly just trade along with the index nowadays. If there are technicals related to index capital flows, stocks like that are going to get taken for a ride.

[1] https://www.etf.com/channels/sp-500-etfs [2] https://www.slickcharts.com/sp500 [3] https://finance.yahoo.com/quote/CB?p=CB

Yes. It has happened before.

Which came dramatically close to happening in 2008, see, e.g. [0].

[0] http://pages.stern.nyu.edu/~sternfin/pschnabl/kacperczyk_sch...

Burry’s money quote in the original Bloomberg article was on limited liquidity for a largish number of stocks - over a 1,000 stocks in Russell 2,000 weren’t traded heavily (by his benchmark).

So what? Let the weak long positions panic and sell at the bottom. Everyone else gets a few years of discount prices to buy. The hardest hit will be those who are leveraged and arguably deserve to get hosed for taking that much risk.

If you don’t have to meet a margin call, you can ride out a crisis; if you’ve got cash in reserve, you can profit from it.

Doing that during a crisis hurts. This risk diminishes the value of investments as a safety cushion.

* https://www.etfstrategy.com/three-reasons-why-indexing-and-e...

See also Vanguard's (biased) opinion:

* https://www.vanguardcanada.ca/individual/articles/education-...

The people using index funds generally don't think about their portfolios—which is the whole point of them. It's probably the cocaine-fueled traders that are causing all the ruckus.

I am not a specialist and would love to read an informed analysis and counters to Burry's article. I was hoping that this is what the author tried (as the title suggests), but to me he fell far short of that goal. My 2c.

This is a smaller example the liquidity problem that Mr Burry was making - it would much worse if a market crash did this to the realy realy big index funds.

When investors sell that amount, it doesn't matter whether they hold the underlying assets directly, or via index funds or ETFs, or via actively managed funds. The market will go down. So, which part of the problem is uniquely due to index funds?

Burry hasn't made that point very clear.

There might be issues with (liquid) index funds that give exposure to inherently less liquid assets, such as bonds or real estate. There might also be issues with index funds that do not hold the assets themselves, but replicate the exposure synthetically by entering a swap with a third party, giving rise to tracking error, counterparts credit risk, etc.

However, as I said, Burry hasn't enunciated these concerns very cogently (at least in the extracts quoted by Bloomberg). This article here does nothing to address those concerns.

In any crisis, the people who get really screwed are those who decide they have to sell, at any price. Instant liquidity - by whichever route - gets really expensive. An actively managed fund can at least decide which assets to sell to meet redemptions, holding those it thinks are undervalued at the moment. Whereas an index fund is effectively exposed to a crisis anywhere in the market.

Further, if there is a stampede for the exits, there still have to be buyers on the other side of the sellers. Those buyers will undoubtably include active managers along with those indexers with different time horizons and/or braver constitutions. Both will likely be rewarded for their patience.

That is a key point in the debate. I do not see that above is necessarily true. Say a price of a low volume stock X is driven down below fundamentals just because index funds have to sell 1% of holdings and cannot find enough buyers for X. While price of X might be irrational fund managers might not be able to act on it because there would be a worry that it may go lower still if selling extends.

Could next round get X removed from index? delisted? "The market can stay irrational longer than you can stay solvent" is not an empty worry. My 2c.

> Liquidity is not a huge problem for index funds. But, Ben, what if everyone rushes to the exits all at once? Index funds and ETFs are going to cause a massive crash!

> When an index fund investor sells, they’re technically selling their holdings in direct proportion to their weighting in the index. So there is literally no market impact.

Yeah, I wanted to highlight that that's not true. Of course there is a market impact, it'll go down. The author might have wanted to say that there is no differential market impact, ie all shares would go down to the same extent (so that there is no impact, say, on capital allocation), but even that is not necessarily true, it clearly depends on the homogeneity (or lack thereof) of the liquidity/elasticity on the other side of those trades.

I'm still driving the price down, causing other holdouts to sell off, driving the price further down. It's the definition of a market crash.

This article does mention it, but pretty briefly.

It'd be interesting to hear from people more familiar with the details of how all this works... perhaps there are some in the initial thread, but I haven't had time to skim it all: https://news.ycombinator.com/item?id=20877700

What is unique about no liquidity during a sell-off driving markets down? It's the definition of a sell-off. The fact there's no liquidity is what drives down the market in every sell-off.

Like my parents did in 2008/9, and I didn't think to caution them not to. Ugggg...

A large number of investors leaving the market will see a sell off no matter what vehicle they're in.

It's hard to see why Mom and Pop buy and hold index investors should care about the liquidity risk Bury talks about...market cap weighted funds will be fine in the long run because the ratio of each underlying stock to a fund share will be constant through the temporary price fluctuations...so no money is lost if the price crashes and then comes back to the same sport shortly after.

Perhaps there are other market participants who are leveraged and would find themselves insolvent if indexes cause a liquidity problem? I just don't see how the fund investors themselves would be hurt if underlying stock prices went out of whack for an afternoon.

The data would also support that on a dollar-weighted basis, most index fund investors are not really buying-and-holding:

"Turnover rates for two of the most popular ETFs are higher than 3500%(!), an average holding period of about a week. That is dozens of times greater than the trading liquidity of even its most liquid constituents"

http://www.grantspub.com/files/presentations/Grant's%20Confe...

Which index fund though? If you're talking about VOO, which follows the S&P500, maybe. If you're talking about VTI (CRSP US Total Market Index), probably less so.

See also Russell 3000 and Wilshire 5000.

Correct me if I’m wrong but isn’t there a well known price premium for stocks included in major index funds? As I understand it, the most popular indexes target a few companies, thus index funds that track them funnel a disproportionate volume of demand to those companies causing a price premium.

It’s stands to reason that if a sudden outflow of money from index funds occurred, that price premium would swing the equal and opposite direction.

To some extent, I'm sure the definition of a "public" company comes into play. Not all stocks are traded in all exchanges, so you could include stocks only listed on one exchange.

Then there's the practice of many index funds picking the top N stocks by market cap. This seems like a backwards practice to me. The small cap stocks should be limited in weight by... their small market cap.

Then there are other hairy factors. Even out of the stocks in an index, it seems that weight does not correspond to capitalization. The reason seems to be some historical drivel. While I can understand that is the way it is, I fail to understand why it should be that way.

Why should an equities index fund be anything other than public companies proportional to their size? If people prefer large cap or small cap, then those variations should be offered as special boutique products. But it seems that we have it backwards, where the default offering is based on arbitrary non-proportional weights, and with a cutoff restricting it to large cap.

VTI is Vanguard's total stock market ETF which works like what you suggest. It has 3,606 stocks, year-to-date it's up 18.82%. Compare that to Vanguard's S&P 500 ETF VOO which is up 19.03%.

When a company hits its stride and is large enough to really make it difference it will join the S&P 500. I guess if there were a lot more than 500 companies that you should own there would be a problem, but we're not there currently.

If you want exposure to small caps it's much more efficient to own an index of small caps. Their performance has seriously lagged in recent times though, so just owning VOO has been the way to go for a long time.

A lot of index funds include small caps nowadays. Not all of them because it's more difficult to track 4000 versus 500 stocks. Also the more popular indexes have usually been around for a long time and have fewer constituents.

>it seems that weight does not correspond to capitalization

Pretty much all index funds invest in the public float and it makes sense:

Maybe the premium is for being in the index, which the index fund dutifully reacts to. There are only 100 places in the FTSE100 so it is seen as significant. The current news about a major UK high street retailer is that it dropped out of this index, implying it's the beginning of its end. https://www.google.com/search?q=marks+and+spencers&tbm=nws

My question is, does this imply that there's substantially more synthetic indexing (without ownership of the underlying securities) than we realize? If there are trillions in indexed assets where the funds owned the majority of the index components, wouldn't average daily inflows lead to higher trading volumes than we're seeing? Or are the market makers such a huge portion of the market that they act as a massive collective buffer causing very few shares to actually be traded?

ETFs are securities that trade freely. They may be open ended or closed ended, but the price of both is determined independent of NAV.

> But it wouldn't move too far because this would attract arbitrageurs who would trade the ETF against the individual stocks and bring it back in line.

This is the creation/redemption mechanism and is actually responsible for keeping the market cap of open ended ETFs in line with the NAV. Closed ended funds don't have such a mechanism, so the cap may diverge from the NAV.

> Another way you could do this is hold a pile of units in reserve and actively sell into the market when the ETF trades at a premium and buy when it trades at a discount. This approach would not result in any volume in the individual stocks (except for re-balancing from time to time).

This defeats the tax advantages of the ETF structure. Instead of having the manager buy and sell names, APs (authorized particpants) do the trading, hedging with units of the ETF. They then do an in-kind exchange with the fund manager at the end of the day. If the AP has net purchased the underlying basket, they will exchange the basket for shares of the ETF (creation). If the AP is net short the basket, they will exchange their offsetting ETFs for the underlying basket (redemption). This should affect the volume of the constituents.

Some ETFs do not require creation and redemption to be done with the full basket of index members. These tend to be based on names that trade less frequently. In this case the manager allows a subset of the index to be exchanged. In this case, the creation/redemption mechanism will not necessarily affect the volumes of all members of the index. Note that this can could cause tracking error.

Managers will rebalance when the index the fund is based on changes. For example, bond ETFs generally rebalance once a month. Market cap weighted ETFs (as opposed to, for example, equal weighted ETFs) are easier for managers as well, because the fund doesn't need active rebalancing.

That would constitute "synthetic indexing" in the sense you are talking about.

He notes that 456 (a little under a quarter) of the Russell 2000 trade less than $1MM/day: "“In the Russell 2000 Index, for instance, the vast majority of stocks are lower volume, lower value-traded stocks. Today I counted 1,049 stocks that traded less than $5 million in value during the day. That is over half, and almost half of those -- 456 stocks -- traded less than $1 million during the day."

S&P index funds have an annual turnover of around 2-4% of AUM typically, so the transaction need to track closely is perhaps not as high as one might think.

Actually, our behavior does shape the price of oranges. If we go to the store and they're less expensive, then we are more likely to buy them. The analogy breaks down because he's comparing indexes and oranges, not stock indexes and food indexes. Imagine if 14% of people went to the grocery, picked up a sack of pre-selected items that were best sellers last week -- all in the name of efficiency and reducing overhead. That would be quite weird indeed, and some people would point out that if enough people did this it would create market inefficiencies and potentially cause a glut or crash of certain food prices.

I'm not sure I agree with this. Most grocery stores stock the same food, so it's not as if going to Lucky instead of Safeway shapes what you can/will get. You're right that if you go for particular sale items, you're more likely to get those. But does that have a basket-level impact? I'm not sure it does. Also, consider that when you go to a grocery store, you probably purchase about .05% of the items they sell. It's not like we go to Safeway and buy most of the things they sell there.

How might we notice that index funds were becoming overrated? Perhaps the rise of hedge funds which consistently outperformed index funds? Is that happening?

What should we do if index funds became overrated? Move our money into a medium-size number of stocks, like 30 of them, to essentially do our own index selection? Or moving out of stocks entirely?

Thinking about questions like this without attacking criticism as “silly” is IMO a better way to minimize risk.

> We’re just seeing a shift from closet indexing to ETFs and other index funds en masse now that investors have wisened up.

So active managers are copying the indexes.

> Index fund investors are simply buying what the active investors have laid out for them.

But indexes buy what the active managers pick.

The author appears to be confused as to who is the tail and who is the dog. Maybe this is resolved by saying some active managers do price discovery, but most are just copycats. It's not clear though.

For the record I think index funds are still the best choice for a retail investor, and the article is mostly true. Namely

> Many of the worries about indexing really boil down to career risk in the asset management space.

Some of the arguments seem to be hasty and not well presented though.

> > We’re just seeing a shift from closet indexing to ETFs and other index funds en masse now that investors have wisened up.

Some active managers used to (clandestinely more or less) copy the indexes, but investors move away from active managers into passive funds.

The prices are determined on the margin, by the remaining active investors. That's all consistent.

> index funds are still the best choice for a retail investor

Yes, index funds or index-linked ETFs. Agreed.

Burry highlighted two simple truths of financial markets: people will buy shit they don't understand, and people who make financial products will try to earn a liquidity premium by transforming something illiquid to something liquid (which always blows up).

Most people (who I have met) who own passives have no idea what they are buying but are sure that buying passives makes them very smart. This blows up every time.

I also don't think Burry was making some bombastic claim about 100% of ETFs causing the end of civilisation. He was making a limited, reasonable claim about trends in markets. Yes, he generalised but, in my estimation, he has earned that right.

Simply, going from 0 to $300m+ earns you that right. Very few people have achieved that. Very few people have done it in the way he did (taking real risk). The views of a triggered financial adviser leeching off his clients don't hold as much weight (and shows all the self-awareness of a financial adviser to write a post implying they should).

If only one person does this I can call him names and downvote him. If there are two camps and both camps do this, people tribalize and everything goes meta. Then no further actual discussion can take place.

There are no "camps" here. The OP is trying to create a tribe (passive investors are cultish, so this is a very odd comment...I will assume an honest mistake) but that makes no sense on this topic (unless you are selling something, which he is).

The meta of my point is: people try this discussion over and over, it is always wrong, some things in finance are universal (because they have been happening for literally three hundred years).

What you appear to have missed is the part where I said: Burry is not making a "bombastic claim" about what will happen 100% of the time. In my experience, most people think this is what investing is about (the OP is certainly an example). It isn't. I am not making a bombastic claim.

The observation is, again, that: you have a lot of unsophisticated buyers and some non-zero amount of these products are about liquidity transformation. You can have a debate about this all you want but it isn't interesting or engaging to anyone but people who are unsophisticated (not 100% true in this case, Asness is a notable exception but he was an academic and it is mostly academics who take an interest).

My interest is limited to the fact that: it is astonishing how often this happens, and equally astonishing how fervently people will deny that it is happening again (although they are usually new converts).

I can't say about the first part, but economically speaking, they are very smart. The alternatives are higher fees and lower results.

"Simply, going from 0 to $300m+ earns you that right. Very few people have achieved that."

You mean the guy who explicitly wants to raise the price of small caps (which conveniently have low volumes)?

(a) have very little skin in the game.

(b) they get to make decisions about what other people have to do with their money

(c) they tend to recommend more stocks with less turnover than typical active managers

(d) they tell the public ahead of time what will be bought or sold, so traders get to buy/sell ahead of time

(e) their actions are relatively predictable, thanks to a long history of sticking to their stated goals.

That said, for all practical purposes it is basically the 500 largest companies.

So if you invest in "all coffee shops" or "all shops in my hometown", you're not looking at fundamentals, you're investing to invest. And, by definition, (assuming all shops are priced correctly) you're artificially inflating.

If someone invests across a group of stocks, it's because "the market always goes up over time." And if enough people believe that then it can be true for a very, very long period. But eventually it becomes your $10 million coffee shop. It's a bubble. And even a bubble that lasts decades will eventually pop.

What I found a little more concerning is their glossing over of the liquidity risks. If everyone wants to sell an index, then at some point that index needs to liquidate shares (proportionally). Those shares won't have uniform demand, which is going to cause both price fluctuations (drops) which affect the value of the index. The fun part here too is that this can play some havoc with market-cap weighted indexes, which now need to adjust their holding %'s.

Traditional money managers may not be the right way to do that, but we should be clear that decisions are still being made somehow.

I guess it's not the investors plowing money into the first index fund they find. And it's not the index fund, because they don't do a lot of management.

So I guess it's a handful of hedge funds that set prices?

As long as a certain fraction of trades are performed by active investors, price discovery will continue to be accurate. Currently, active traders dominate, making up the majority of trades. This fraction could be much smaller than it currently is and still be OK.

Are we sure that the right model is to just watch these first-movers and do what they do?

Active funds literally own the market. When you buy an index fund of the total stock market, you are literally buying the stock market in proportion to the shares held by all active investors. If you sum up the collective holdings of active managers, what you basically get is a market-cap-weighted index. Index fund investors are simply buying what the active investors have laid out for them.

I don't have the knowledge to evaluate this statement, but to me, it undermines Burry's point that passive investing distorts prices.

And this bit that he quotes from someone else expands on the point:

The use of price signals by those who played no role in setting them may be capitalism’s most important feature. That most of us and most of our dollars don’t have to pick stocks, or to price air conditioners, is a great benefit and taking advantage of it makes us honest smart capitalists, not commissars.

As I understand it, Burry's argument is that index funds distort prices because capital is being allocated in an automated and uniform way, instead of being allocated according to the expertise of a diverse, success-weighted group of investors who are motivated to make intelligent and informed decisions. At some point the difference between the index-fund-driven prices and the "true" prices according to informed opinion will become obvious, and investors will attempt to flee index funds, popping the bubble. The rebuttal in this argument is that active investors are still controlling the market because index funds mirror their activity. We will never reach a state where people will rush to "escape" from the index funds to actively managed funds, because index funds will always approximate the aggregate opinion of the actively managed funds.

This accords with my naive idea of how index funds work, but I don't know if they actually do work that way, so I can't evaluate the soundness of either argument.

That works until it doesn't. If passive becomes big enough, the indices themselves will be the ones steering the ship. The active managers won't be significant enough to sway the indices.

I heard this analogy on a podcast (I think it was Invest Like the Best): Indices are like a drunk person, and active managers are like the sober friend guiding the drunk home. But if the drunk becomes 10x the size of the sober friend, the friend is no longer strong enough to be a guide.

If passive funds get big enough to dwarf active management, they eventually will be the ones steering the market, and active investors will be noise at that point. In that scenario, I'm not sure what happens, but it seems that indexing would become more like a Ponsi scheme.

Also he jumps around Burry's arguments by focusing on liquidity and in AAPL and FB. Burry's whole point is about less liquid components at the bottom of indices which are getting dragged upward by a lack of price discovery and inclusion in widespread passive funds. Since they're market-cap weighted, this would have a cyclical component, more passive purchases -> higher market cap -> higher weighting in passive indices -> more passive purchases. This would result in another cyclical component where that cycle causes: passive fund outperformance -> increased investing in passive funds -> passive fund outperformance.

Then in an event where people start liquidating there is no one there to purchase those stocks and they've been dramatically overvalued anyways so their price gets crushed. This is specifically why Burry likes small cap active.

If you pay attention to finance discussion on this board then you've definitely heard the phrase: “The market can stay irrational longer than you can stay solvent.” The argument here is that irrationality has persisted long enough to crush most 'rational' price discoverers.

>Do you know what didn’t cause the Great Depression or Japan stock market crash or 1987 crash or 1973-74 bear market? Index funds. Index funds also weren’t around for the South Sea bubble in the 1700s. Do you know what did cause these bubbles and subsequent crashes? Human nature.

Imagine doing this but replacing 'index funds' with mortgage CDOs.

Look I'm not even saying Burry is right but the absolute inability of the finance commentariat to actually address what he's saying is giving him more credence.

If prices are being set predominantly by active investors who are truly buying and selling based on bottom-up, security-level research, then the percentage of assets that happens to be invested in passive funds is not that important, because price discovery would be working exactly as you and I would hope.

But if prices are being set predominantly by (a) active investors who are chasing indexes because they don't have a choice, (b) active managers who are being forced to sell positions to cope with a high rate of redemptions (from investors who plow that capital back into passive strategies), and (c) traders who grasp this dynamic and shrewdly exploit it for as long as possible; then price discovery might not be working as we would hope. Prices would no longer be reflecting perceived risk; they would be reflecting the (temporary) influence of this once-in-history dynamical process.

Burry makes a compelling case, I think, that the latter is a more accurate description of the current state of financial markets than the former, and that this state of affairs can only persist so long as capital continues to flow from active to passive strategies at such high rates. Globally, assets under management are not infinite, so capital cannot flow indefinitely from active to passive strategies: Sooner or letter, this dynamical process must exhaust itself.

I don't know what other ETFs have in their prospectuses, but this wiggle room seems like it could mitigate some of the concerns about crashes due to low liquidity in thinly traded stocks.

[1] http://hosted.rightprospectus.com/ETF/Fund.aspx?dt=P&cu=8085...

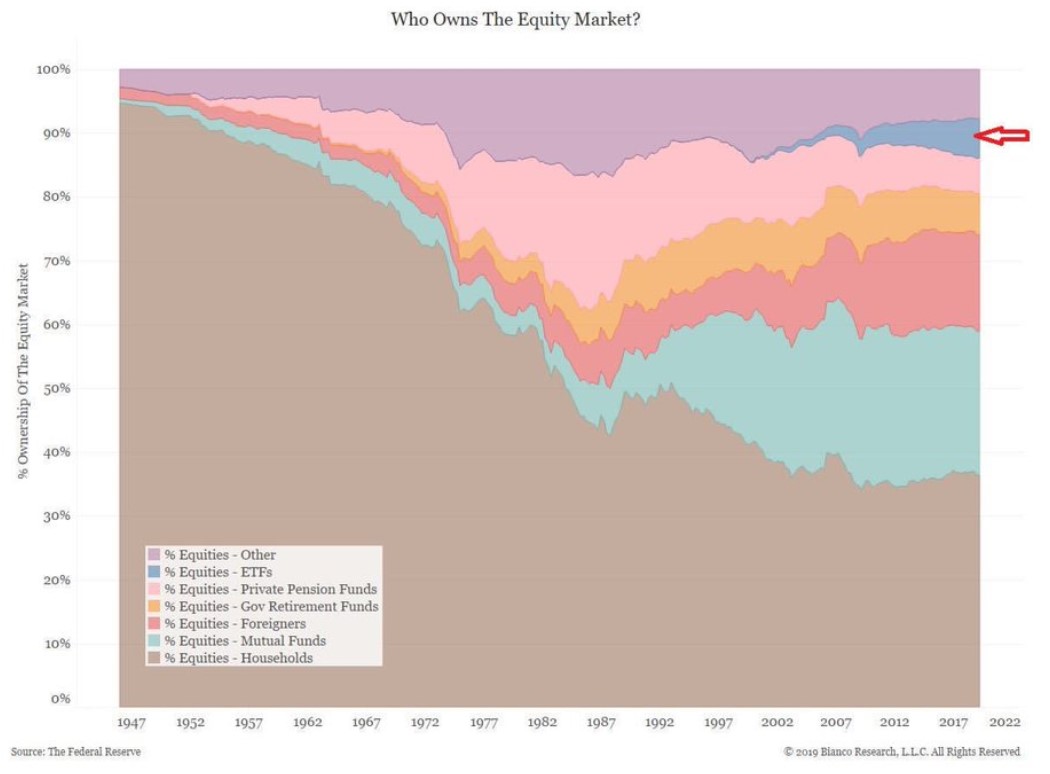

His graph shows an arrow pointed at the small sliver on ETFs, but that isn't necessarily the same as passive investing which would include a lot of mutual funds.

Have to take the rest of the article with several grains of salt after reading this. Even if the index was spread against all stocks it would have an impact. It implies that you can only move money around the market, not take it out of the market altogether.

My mother-in-law works for the state doing financial investing, and I've seen some of the functions and constant values she's had to memorize to get her degrees. Constants that are based on models that are often decades old. It's all ultimately a form of forecasting based on models, but it's treated as gospel of how it will all occur.

Perhaps that's why it works at all - everyone's using the same models, and they behave in a set pattern (established by schooling and "how it's always been done") based off those models, which makes the models accurate.

If i were king for a day I'd legislate a low bar that required the equities to be listed so that both the insiders cannot be barred from liquidity and so that the investing public can access those parts of the economy.

The problem with those arguments is the fact that what turns a recession into a depression is demand strikes: when the people with cash lose faith in the integrity of the market, they just take their money off the table and go home. Arbitrage and market correction dynamics cease to function.

The fact that depressions can be caused by collapses in demand as well as in supply was the key insight of Keynes et al. in the 1930's, which is why he argued that the government must have the power to regulate markets and the authority to step in and become the buyer of last resort in the face of an incipient depression.

Keynes' insight was conveniently forgotten by the early 2000's, regulation was resisted, the shadow market grew out of bounds, bailouts and stimulus met political resistance, and the rest is history.

How short the time span of memory is.

Anyone have suggestions on the best sustainable ETFs out there?

Economic systems are feedback loops. If something is the best investment that causes it to become a bad investment in proportion to how rapidly people realize it's a good investment.

http://www.grantspub.com/files/presentations/Grant's%20Confe...

Edit Some highlights:

> Does an asset allocation program or roboadvisor tool seeking foreign market exposure know that 6 of the top 10 holdings of the iShares MSCI Spain Index get 70% or more of their revenues from outside of Spain? That a purchase of the ETF is, essentially, investing outside Spain? The same holds true for emerging markets ETFs.

> the business demand of ETF organizers for liquid stocks has only increased, with the influx of funds directed into the same limited population of liquid stocks. ExxonMobil is one of the most liquid. Ergo, it will be found almost anywhere one can imagine that it can be placed. It’s Growth, It’s Value, Its’ a Bird, It’s a Plane...

> Would an active manager of a low-risk strategy be permitted the risk of a near-50% weighting in financials? ... These largest-in-class ETFs can legitimately be characterized as low volatility, since of late the financial sector has not been volatile. And the high weighting enables the ETF to attain its advertised low Beta.

What's unclear is the impact that ETFs have on prices. This "debunking" doesn't address the point about low volume.

Let's suppose most of those non-ETFs owners are buy and hold investors that bought in a long time ago and wouldn't buy anywhere near today's prices.

That would mean ETF holders, especially those who joined late, could still be responsible for a disproportionate share of today's prices. If the market shows signs of weakness, these people need to get out, especially if they bought on leverage.

Apple alone has $50 billion in cash that will flow into Vanguard if index funds hit a 50% plunge. Same with Buffet. Index funds may be bubble priced, but they don't suffer from a liquidity issue.

This is a straight out false statement. Who is this guy again? Oh yea, he has his hands in passive investment big time.

If you believe, for instance, that there is an "S&P 500" bubble then there is difficulty turning that into an investable thesis. The S&P 500 is about 80% of the valuation of the stock market. If the S&P 500 pops, then relatively the other 20% of the market will go up, but how much can it go up?

The most harmful effect we know now of the passive funds is that they have a strong incentive (when they vote their shares) to discourage competition. If they own both AT&T and Verizon they would rather both of these be profitable at the expense of consumers rather than work hard to gain market share for one or the other.

{kind=link}