There are two things that make the current banking system robust: first, because anonymity is limited, most of the actors in the system are honest. Trying to pull a fast one is risky, and that prevents most people from trying. And second, there are humans in the loop that you can appeal to when things go wrong. Most of the time this keeps the system humming along despite the fact that under the hood it's all held together with spit and baling wire.

Bitcoin is the exact opposite. Because it provides greater anonymity than the traditional banking system, it attracts dishonest actors. For example, bitcoin has made ransomware more economically viable than it was before. And second, if something goes wrong with a bitcoin transaction, you are totally hosed. Your bitcoin payment is only as safe as your ability to reliably bind a bitcoin address to an intended recipient. If you get it wrong, there's no recourse. If you accidentally send some bitcoin to the wrong address, you are hosed. If you lose your private key, you are hosed. Period, end of story.

If I have to choose between bitcoin and traditional banking I'll take the latter simply because it's generally more robust and forgiving of everyday human foibles. But I'll continue to wish for (and work towards) a system that gives us the best of both worlds.

Bitcoin should be seen as a currency first and a payment system second. Nothing should prevent the current banking system from adopting it as a currency while keeping all their existing checks in place. Credit cards could support BTC denominated payments and still have all of their chargeback policies in place.

In that world, doing a large Bitcoin transaction would be the analogous of moving trucks of cash around and keeping a large amount of Bitcoin would be like hiding tons of cash in under your mattress (reserved for experts). The majority of payments would be "off chain" while still allowing for people to opt out.

You might ask what's the point of Bitcoin then? Well, I think it would still have a couple of benefits over traditional currencies like USD:

- Supply of currency not controlled by any government or entity

- Easier to "opt out" from system than with physical cash

- Transparency (institutions that wish to do so could use the blockchain to be transparent about their finance)

- Efficiency (though there's been a lot of criticism about the energy consumption of Bitcoin mining, think of all the human capital, real estate and transportation cost that goes into physically moving and securing cash)

This doesn't apply if many of the transactions happen "off chain" to offer the reversibility benefits you mentioned before.

Basically, to get all of the trust benefits of the banking system, you are saying we have to essentially not actually use bitcoin, which makes me wonder what the point is. At that stage, why not have gold denominated credit cards? Less technology to depend on and the government still doesn't control supply.

Well not these guys: $81M was stolen from the Bangladesh Bank via the SWIFT network in February https://en.wikipedia.org/wiki/2016_Bangladesh_Bank_heist

> And second, there are humans in the loop

There sure are!

The IRS Seized $107,000 From Store owner for "structuring" http://www.foxnews.com/politics/2015/05/12/nc-store-owner-on...

MasterCard Cuts Off Wikileaks, Assange's Bank Account Frozen http://gawker.com/5707851/mastercard-cuts-off-wikileaks-assa...

DOJ's 'Operation Choke Point' May Be Root of Porn Star Bank Account Closings http://reason.com/blog/2014/04/28/doj-operation-chokepoint-a...

Nearly all of which was later recovered.

> The IRS Seized $107,000

> DOJ's 'Operation Choke Point'

Those are political problems, not problems with the banking system. If the government decides to fuck with you, then you're fucked no matter what the banking system looks like.

> MasterCard Cuts Off Wikileaks

This is a real problem, and it a result of what is IMHO the main unaddressed flaw in our current system: banking is conflated with money transfer. Bitcoin does address this problem, but IMHO it doesn't do it very well. The risks and costs are too high.

He got it back eventually plus $20k costs http://www.cato.org/blog/lyndon-mclellan-finally-beats-irs

Although this is true, the fact is that in practice this is rarely occurring. No system needs to be absolutely perfect to compete reasonably with the legacy financial banking system. As you point out yourself, the banking system has flaws, and yet it kind of works. Ditto for Bitcoin: it's not perfect, but it works quite well at solving certain real-world problems.

I think theft of Bitcoin private keys is a more serious problem than accidentally sending coins to the wrong address, however this is being solved by hardware wallets, N-of-M transactions, etc.

Mainly because wallet spoofing is not yet lucrative enough for hackers to put a lot of effort into it. If BTC really does start to get major traction, then it is only a matter of time before the web will be flooded with bitcoin wallet spam and phishing attacks.

If you look at it from high above, it would be like replacing the implementation of the current banking system with a more modern stack, but still leaving a similar human interface with the same level of features.

Would this make sense?

There are some people arguing in this direction, with the construction of settlement blockchains, but obviously the proof-of-waste system would have to be discarded.

I think the Right Answer is to have an auditable public ledger maintained by a trusted third party. This could be the government, or it could be a private party, but the key to making it work is to make electronic money storage and transfer a commodity provided by what is essentially a public utility.

What problem does bitcoin solve for banks?

Maybe im being totally naive.. but how about a second blockchain called the "rollback" blockchain.. Suppose you put a "timer" in the bitcoin blockchain for a period lets say 48 hrs..

So when the timer expires, the first blockchain(the coin blockchain), would check for a "rollback transaction" in the second one.. if its not there, the transaction on the first blockchain would be confirmed, and the funds would go to te right account, in a completely automated way, with all the trust garantee that the blockchain tech can give.

Is this a stupid idea? (i just gave a quick tought about this)

OBS: of course, say goodbye to instant payment.. but with double check security sugar on top of it.

https://en.wikipedia.org/wiki/Smart_contract

And for a cryptocurrency-specific implementation, see http://nashx.com/HowItWorks

Of course you could try, but (I predict) you will fail. The problems I've cited are fundamental problems that are built in to the bitcoin protocol by design. You can't patch your way around them.

For example:

> which has nice UI and double checks everything

How exactly are you going to "check everything"? Remember, you have to get it 100% correct. Failures are completely unacceptable because failures are completely unrecoverable.

This is a strange argument to me. There's plenty of community credit unions around. For trust you can walk right in and speak to the manager. Some of them are older than dirt.

However there's nothing really new in these fears (especially after 1929). The solution has always been to keep your money locked up in a safe. Pay for things in cash or cashiers check.

In a way, it reminds me of the ol' Reflections on trusting trust (https://www.ece.cmu.edu/~ganger/712.fall02/papers/p761-thomp...), but in a somewhat broader sense.

For my part, really, at the end of the day, I'd sooner trust institutions that have been around for a long, long time (far longer than I've been alive so far) than a coding project that's been around for less time than most of the popular websites I read.

But it'd be a funny old world if we were all alike, of course.

You are never safe against the risk of fiat money devaluation, though (or even folks breaking into your home and stealing your safe). Of course, the devaluation risk exists with BTC as well, but at least it does not depend on a central government.

And there's also the risk that, as newer notes and coins come with stronger anti-counterfeiting measures, older notes and coins aren't accepted anymore, or accepted only with a discount over their nominal value. (I've seen it happen with older USA dollar bills left over from a trip to the USA a couple of decades before.)

At least the fed has the bureaucracy and some manner of legal system keeping them in check!

Don't say "forks" either - we may or may not be at the point of maximum entrenchment yet, but requiring literally every BTC user in the world to update their software for their money to work is unrealistic.

I'm quickly coming to the conclusion that bitcoin is about as perfect a medium of exchange as you will ever get (immune to censorship, immune to legislation), but is comparatively awful as a store of value.

His point with BTC was that you didn't even have to trust some manager.

>However there's nothing really new in these fears (especially after 1929). The solution has always been to keep your money locked up in a safe. Pay for things in cash or cashiers check.

How do you pay with cash online?

If you wanted to avoid even that amount of storage, you can also use them primarily for borrow money(credit cards, loans, mortgages, etc.) and pay the debts back with cash. I can access borrowed money through my bank's online interface.

Bitcoin eliminates the need to trust some 3rd party human beings with your money.

BTW what does being "older than dirt" have to do with being worthy of trust?

Unless you are also auditing all the code you use for software that objects with Bitcoin yourself, it also requires trust in either the software developers or other people who purport to be auditing the code.

The idea that Bitcoin eliminates the need for trust is a dangerous delusion.

I think this is stupid in the extreme, and you SHOULD NOT do this ever.

Bitcoin is super interesting as an asset vehicle, but I would not put all my eggs in that basket. For as much as I might not like the Fed and some of the monetary policy it makes, it still gets things done. Right now bitcoin can't seem to change the block size, it needs to, and a squabble could cause serious devaluation of the product as a whole.

There is also the ticking time bomb of the satoshi coins. Right now one individual (or group) controls something like 6% of all the coins available, and on a whim, could cause a major devaluation over night.

All this having been said would I consider buying and holding some bitcoin as very LIQUID asset, and cash equivalent. I sure would. How much would I put into it, no more than a few grand honestly, a sum I am willing to loose.

The Fed does this on an annual basis and actually publicly states when it's going to devalue the currency through QE and rate cuts.

No, your one vote won't change everything to suit your personal preferences, and if you wanted to change the way some aspect of our system works (like money, or health care, or drug policy, or whatever) it'd be a lot of work, consensus-building, and time. But, at least the power is in our hands, collectively.

(Offtopic) And, sorry, I had just fat-fingered a downvote when I meant to upvote!

Edit: also, systems that are private will get you in trouble with KYC/AML.

But how liquid Bitcoin really is?

Suppose you have 1 BTC on your phone. Can you instantly turn it into cash (and vice-versa)? Does that depend on a single Bitcoin exchange, which can stop working suddenly leaving you stranded? Does it have to go through your bank account or your credit card account?

This is probably not an issue if you live in a place with a high enough amount of Bitcoin users, since many of them could be willing to exchange Bitcoins and cash with you. But otherwise, it's a relevant question to ask.

Is it more liquid than the stocks I own, yes, and those are the most liquid of my investments (vs bonds, 401k etc).

I live in CA so I have a rather large chunk of cash on hand. It isn't outrageous amount, but I could make it for two weeks if there was an earthquake or natural disaster. I don't think the bitcoin would do me any good if that happened.

That is a strange argument. The value of Bitcoin comes from the trust people have on Bitcoin. If nobody trusts Bitcoin, it's worthless except as a mathematical curiosity.

And after just a few more paragraphs, we see another instance of trust. The author describes leaving most of the money in a hardware wallet. That is, the author is trusting that the hardware is neither malicious nor buggy. A malicious hardware wallet could use kleptographic attacks to exfiltrate the private keys, or derive them from an attacker-controlled seed. A buggy hardware wallet could, for instance, have a "stuck" RNG (like a well-known OpenSSL fiasco), such that the generated private keys are predictable.

The author is trusting people he doesn't know: the designers of the hardware wallet, the manufacturers of the hardware wallet (including workers at whichever factory manufactures the hardware), and even the postmen. Moreover, the author is not only trusting them to not be malicious, but also to not make mistakes (with crypto, even small mistakes can be deadly).

And there's also at least one other problem the author didn't consider, or at least didn't mention: inheritance. If the author has an accident, what happens to the money? And what if the accident is not fatal, but leads to neurological sequels which render the author unable to access the hardware wallets?

> have a "stuck" RNG

TREZOR asks for external entropy during the initialization and this one is mixed with an internal one. Even in the unlikely change that internal RNG generator fails, you should be on the safe side.

> The author is trusting people he doesn't know

The whole design is (hardware and software) is open-source. You don't need to trust, you can verify yourself (or ask a friend who can if you are not able to).

> inheritance

When you initialize device it will give you a list of 24 words, which are a way how to recover funds. You can split these words across your family members (using e.g. a Shamir's Secret Sharing Scheme) and once you are dead your family can recover your coins.

I recommend watching my talk at CCC where I explain in detail the basis concepts of TREZOR: https://www.youtube.com/watch?v=CgaBKNus1n0

Assuming it actually uses it.

>The whole design is (hardware and software) is open-source. You don't need to trust, you can verify yourself (or ask a friend who can if you are not able to).

This doesn't matter unless you build it yourself. Open source hardware and software specs are irrelevant if you have no proof the thing you are using followed them precisely.

If Bitcoin was closed source, I'd agree with you.

But it's not, and I don't. Bitcoin is 100% transparent and reviewable: the code, the transactions. The same cannot be said for any national or bank electronic monetary system.

As a technical person, I'd trust an open source system more than closed source system any day of the week.

You just said it: you trust. You trust Bitcoin because you can (and perhaps already have) review the code, the theory, the blockchain. But it's still trust, and you probably value Bitcoin only because of that trust.

Edit: Apparently on first use the device displays a list of recovery codes which would cover it being lost and the inheritance issue (assuming the manufacturer is still around). I'm a bit concerned the recovery is through a web based tool though:

The recovery is through a web-based tool, but the order of the words is randomized and displayed only on the device, so even if someone installs a keylogger on your PC, he would need to know the correct order (since it's 24 words, that's safe enough).

(Disclaimer: I work for SatoshiLabs, the manufacturer.)

Bitcoin is like cash, not like a credit card or bank account.

"I do not accept the concept of “trust”" Right Cashila.com/BitWage.com are operated by magic trustworthy unicorns.

I think you still trust those services with your money in the same manner you trust classic banks - no real difference here, both can be used just for transfers and not keeping anything with them. Except for with banks it's really tiresome and inconvenient to load on demand and with Bitcoin it's nearly a one-tap experience.

There is this group of people that had higher education and are well versed in system security, they are called sys admins and even they get hacked some times... but here you are trying to convince us to put all our money into easily movable and untraceable bits in some bitcoin wallet claiming it it the safer option we have.

I get that you're not a fan, but exaggerations don't enhance your argument. Over the last 60 days the XBT/USD pair has an average volatility of 1.23 % [1] which is obviously higher than most major currency pairs, but comparable to a many stock markets. That is, many people invest money in securities with similar or greater volatility profiles.

> easily stolen by some hacker

Whilst Bitcoin is obviously less user friendly than fiat currency, an experienced user like OP can make store their Bitcoin in a way that makes it much more difficult to steal than conventional payment systems.

Firstly, using a hardware wallet (with offline backup) will make your Bitcoin almost invulnerable to 'hackers', plus the use of multi-sig can allow one to dial up physical security to very high levels.

Compare that to conventional payment systems like a credit card - all your credentials are on your card! Anyone who handles your card (waiters, cashiers) gets access to all of your credentials, for the life of the card! (Bitcoin's use of public key cryptography is far more sane in my opinion). And any malware on your computer that could steal Bitcoin could also steal your CC information etc. The only reason that this isnt more of a problem is because by using a bank you are paying insurance for your money and the Bank will generally reimburse you for small amounts - this doesn't make the conventional payment system more secure, just more insured.

1st. It's not the average volatility that matters it's the maximum volatility that you can normally have. This year it only happen once to have 20% it's true. But you have plenty of days where it oscillates more than 5%.

2nd. Bitcoin is much easier to steal than conventional payment systems like reality tells us, not only because of it's lack of security but also because of accountability. It's hacker free reign, you just steal bitcoin and send it anywhere you want and you have no more trouble. In traditional payment systems this doesn't happen like you try to imply, not because it's insured but because we are talking about real money and that money is connected to a name and an address and sooner or later the police will knock on your door or the door of the person that received the goods purchased with the stolen money or card.

3rd. "Firstly, using a hardware wallet (with offline backup) will make your Bitcoin almost invulnerable to 'hackers'": In a site like this dedicated to people that actually understand a bit about computer security. this sentence is just funny.

Residents of e.g. Brazil and Argentina are entitled to a different opinion due to different history, but in those countries people sought hard currency .. the dollar.

The Euro may not be perfect, but at least there are rules and institutions working to prevent this happening again.

We gave it symmetrical gerunds.

Edit: on second thought, "hacking yourself out of the banking system" is kind of baity and doesn't seem to add information, so we'll take that out.

Which tense do you want to live in ?

— I want to live in the imperative of the future passive participle— in

the “what ought to be.”

I feel like breathing that way. That’s what I like. There exists such a

thing as mounted, bandit-band, equestrian honor. That’s why I like the

fine Latin “gerundive”—that verb on horseback.

Yes, the Latin genius, when it was young and greedy, created that form

of imperative verbal traction as the prototype of our whole culture, and it

was not the only thing that “ought to be” but the thing that “ought to be

praised”—laudaturaest—the thing we like. . . .

..The Prose Of Osip MandelstamI also know of a (small but consistent) linguistic practice in which people deliberately speak in gerunds as a form of verbal indirection, and it works surprisingly well.

This is INSANE. Justifying monthly 30% swings in the value of your currency with "bank fees suck" is complete nonsense. Currency instability like that destroys economies because people lose the ability to budget and they become fearful.

In the worst periods of inflation in the US, the currency never devalued by 30% in a month. That's Zimbabwe level crazy.

Also, I pay precisely $0 a month in bank fees, as do many other Americans, so that argument would fall flat even if the swings were much smaller.

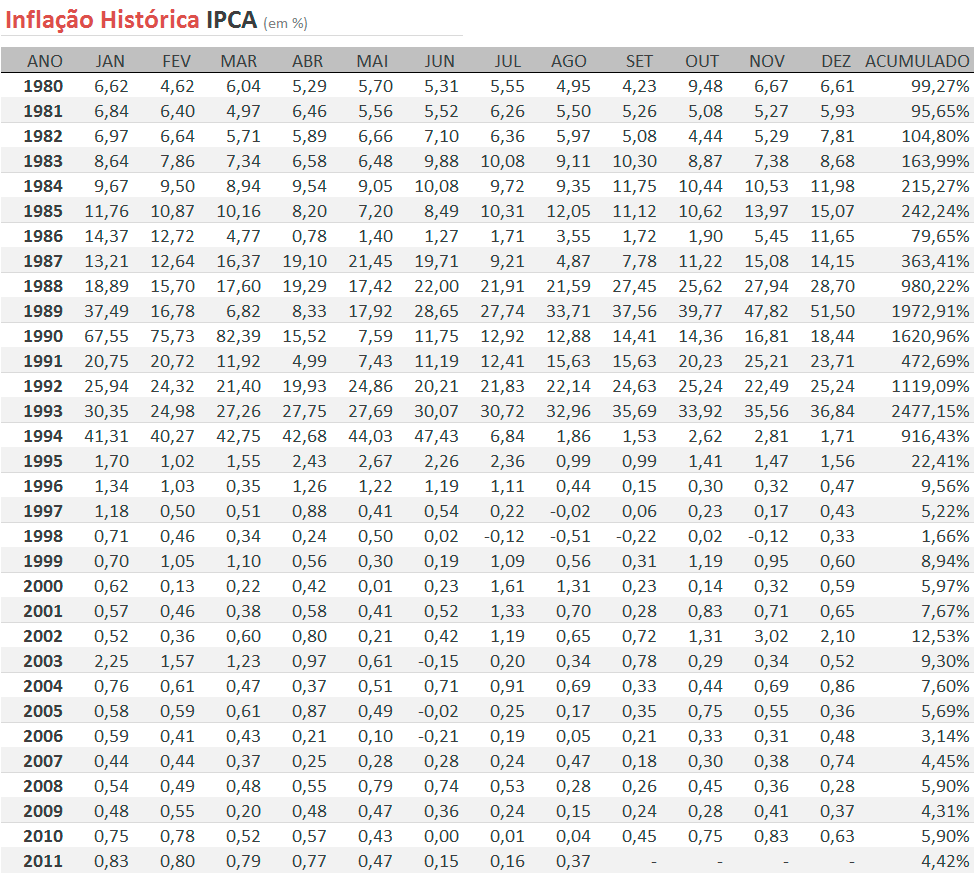

I've lived through 30% a month inflation. See the table at http://hcinvestimentos.com/wp-content/uploads/2011/02/IPCA-I... (source: http://hcinvestimentos.com/2011/02/21/ipca-igpm-inflacao-his...). At this level, people can still cope, but it does generate some distortions. For instance, as soon as you received your monthly salary, you bought all the food you'd need for the whole month. If you can read Portuguese, I found an interesting article about it at http://www.bbc.com/portuguese/noticias/2014/06/140619_plano_... .

Also, when you analyze the details you can discover that using https://cryptopay.me/bitcoin-debit-card takes extra commissions beyond bitcoins (loading fee 1%), so the magic of bitcoins fade a little bit.

Just the other day I came to the conclusion bitcoin is a monitoring tool for the powerful to keep track of advances in digital security by incentivising implicit disclosure.

If someone cracks integer factorization or tsp and thinks bitcoin would be a great way to make some dough on the discovery it will immediately set off red flags to anyone watching.

If your typical nonce is found in a pool of many, but an individual suddenly starts solving blocks and banking 25btc, as of this writing, left and right you'll know straight off that individual has compromised the entire system.

Putting a target on the poor rube's back and destroying any confidence in bitcoin as a currency.

Perhaps this is unlikely but to put all of your trust in a system with such a huge potential to immediate failure terrifies me.

Who is satoshi? Maybe a three letter acronym.

The gateways (fiat->btc, btc->fiat) know your identity, take a higher fee than banks and you still have to trust them. Additionaly, you now have the risk of varying exchange rates at multiple points in your money flow.

As for the global bitcoin adoption, I don't see this approach helping at all. If you think of yourself as a node in a global economy graph, you still take fiat as input and produce fiat as output.

does this include a larger desire to spend BTC (because of wanting a value store, for example) compared to USD?

{kind=link}