A significant part of the broker's value is the high-touch relationship and trust.

The market fit question to me is: if a state marketplace has a decent web portal (like California's http://www.coveredca.com ), what additional value does a private portal offer that NEITHER the official portal NOR an offline broker can offer?

(Don't mean this as polemical by any means; lots of states are not going to have great portals. Just interested in hearing opinions on this.)

[Edit: making CA link a real URL]

Some examples off the top of my head:

- A healthy 24 year old software engineer is making $75,000. This means he doesn't qualify for any of the tax subsidies by buying insurance on the exchange. He wants to avoid the $2,500 penalty for being uninsured, but every plan on the Covered CA will cost more than that over 12 months. Perhaps his best option is to buy an individual policy for catastrophic coverage only.

- A small business isn't sure whether it's optimal to insure their employees, or just give them a cash "bonus" and tell them to buy their own policy on Covered CA (similar to what Trader Joe's announced they're going to do with their part-time employees).

- Purchasing insurance on Covered CA is limited only to certain enrollment periods (this is perhaps the biggest misunderstanding, as I've seen various media personalities ask "why wouldn't healthy people just wait until their sick, and then get insurance?" countless times). However, there are exceptions for a life-changing event. Thus, a person who is laid off (thus counting as one of those life-changing events) would like information on whether their best option is to pay for COBRA or buy a policy on Covered CA.

Basically the ACA is complex, but it does turn health insurance into a much more structured and transparent market, which lends itself well to applications like SimplyInsured. Otherwise, what could any sort of system do for my third scenario, for example? All anyone could advise to have them stay on COBRA because they'd probably get screwed by letting it lapse and then trying to get an individual policy.

The chart under Question #2 - answers your question.

There's a role in the government for insurance regulation, however companies like SimplyInsured are needed to actually execute.

This is FedEx vs. the Post Office.

Yes, California is a much larger market, but the Massachusetts exchange has been up and running for years. Given that, it seems obvious to me that, for now, Massachusetts is a far better proving ground than any other state for a health insurance business.

Some previous colleagues of mine just raised 2.6M a couple of weeks ago [1] for a very similar sounding idea [2]. This is a hot space right now with all of the attention on health care because of the ACA and all of the failings of the public exchanges in the press.

[1] http://www.bizjournals.com/twincities/blog/in_private/2013/0... [2] http://www.gravie.com/

I'd much prefer we don't devolve into a political argument. My question, I thought, was relevant due to ACA kicking in, which is the first step towards universal healthcare/single payer in the US (which would eliminate the business model in question).

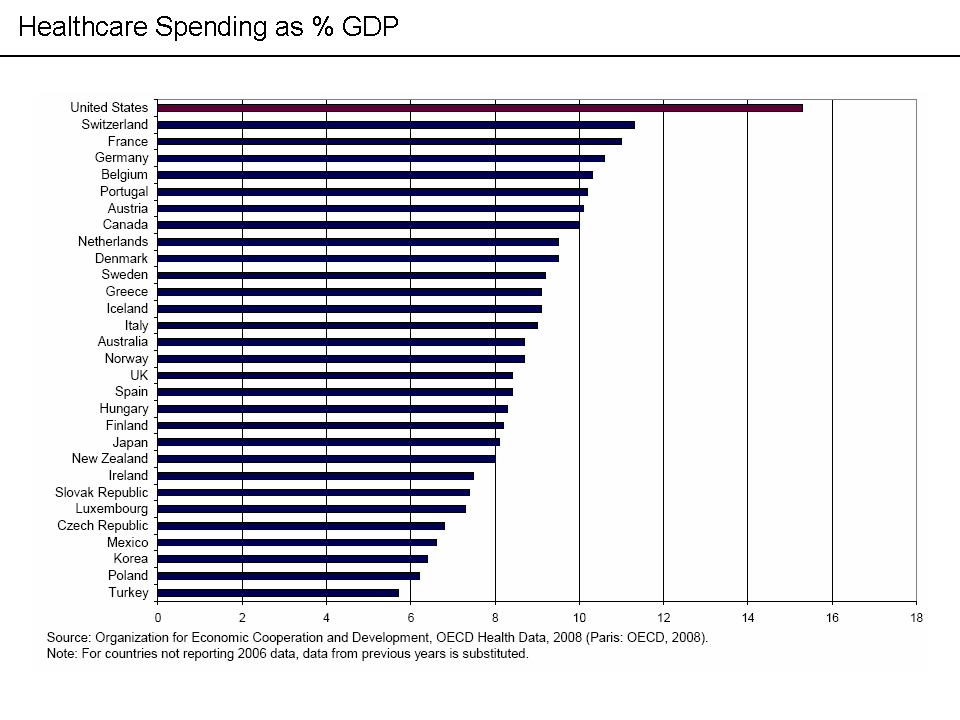

In closing, here is healthcare spending as a percentage of GDP by country (almost all first world countries): http://upload.wikimedia.org/wikipedia/commons/a/a1/Internati... The US leads in spending, and only spending.

Maybe if you live in opposite world; in this world, it does exactly the opposite.

The weird thing about ACA is it essentially turns this into a relatively low range problem; I'm going to be spending $200/mo to $400/mo in premiums, and I'm never going to be out of pocket more than $6350 on top of that. So even if I do exceptionally well, it's maybe a $200x12 - $3300x0.35 (tax savings on HSA) cost vs. a $400x12 plus epsilon cost vs. ($200x12 + $6350). Which isn't enough to really care that much, since most likely it's within $1-2k/yr regardless of which plan I pick. And I doubt your picking would be that much more accurate than a general WAG based on "do I often go to the doctor?"

{kind=link}