What is the most definitive evidence (actual data plus analysis by economists) that you can point me to that proves this is true?

Not all of that housing is where people want it, investors are collecting properties like Pokémon, the vast majority of people can only afford a house half the price they could before interests rates rose, and those with mortgages are stuck with their low rates and little incentive to move (or at least sell).

So it’s not the lack of units that’s the issue, but a market that (surprise!) favors the wealthy and entrenched. If you had cash, houses could be found at absurdly low prices 12 years ago. But as always, the climate favored the wealthy whose credit score wasn’t wrecked, who had excess capital to deploy, and were willing to tie it up in real estate for 5-10 years as the market recovered.

0 - https://twitter.com/Econimica/status/1686999658483314688

Desired household sizes keep decreasing due to ongoing drops in marriage and childbearing rates, which increases housing units out of historical proportions.

This is compounded by the desire for vacation homes and the continuing opposition to increased housing in privileged areas such as the coastal cities.

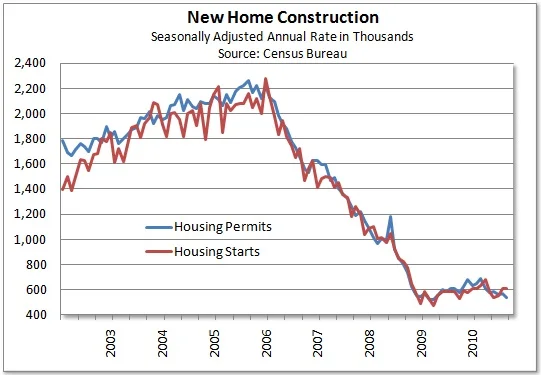

Here's a fun graph from the US Census Bureau:

https://images.squarespace-cdn.com/content/54683a71e4b0768e1...

Also the numbers do not exactly support your statement: https://www.construction-physics.com/p/is-there-a-housing-sh...

I bought a home last year during peak sales season in a great neighborhood in a major tourist town at a very reasonable price that had been on the market nearly a week before I made my offer. How? Because my HOA explicitly forbids me from using the home as a STVR, which kept most interested buyers away. The desire to capitalize the house in the future is a major factor in rising home prices. I can do a long term rental, but no Airbnb.

Want to dramatically reduce upward pressure? Start passing laws that severely punish STVR activity and prices will come down.

Case study: Vancouver, BC, Canada (I looked in May 2023). House prices: ~$1.1M. Loan rate: ~5%. Month payment: $5900. Yearly: $71k. Avg Salary: 60k (before tax). Result: No normal worker can afford the loan, and the bank won't give you the loan.

When interest rates sharply rise, suddenly all loans to normal humans based on existing prices look like failure, because there is no way to make the payments. "I'll give you a loan, so you can miss payments every month, owe me more every year, and then default. No." if( money_earned < monthly_payment) then { no_loan }

Also, wealthy need somewhere to park their money. A bunch of really wealth folks made a bunch of enormous profits last year. [2] Frankly, if you're in the $10^9 club, there's not much to buy. Personal air craft carrier? Your own airforce? Build your own town? [3] Reconstruct all of Iraq? [4]

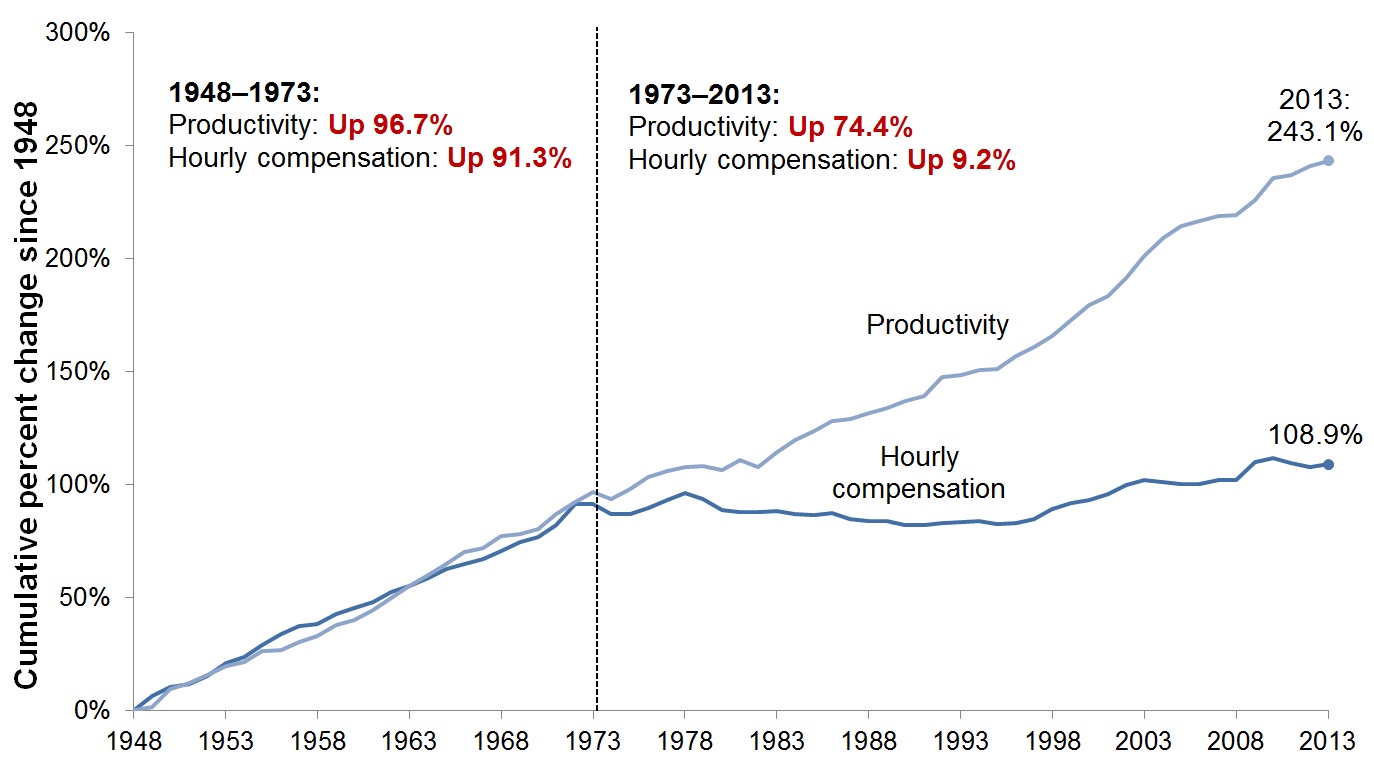

[1] https://files.epi.org/2013/ib388-figurea.jpg

[2] https://www.reuters.com/business/energy/big-oil-doubles-prof...

[3] https://thehill.com/homenews/state-watch/4184337-california-...

[4] https://www.google.com/search?client=firefox-b-1-d&q=reconst...

https://www.vancouverisawesome.com/local-news/vancouver-rank...

Vancouver, especially, has not seen salary gains in keeping up with the housing market. It is explicitly, unambiguously, huge amounts of foreign money. The housing prices in greater YVR correlate to foreign issues in China like Xi's crackdowns, or MBS' takeover in Saudi.

This is true for Greater Toronto as well, but very much less so over the rest of Canada.

This is nonsense. The US treasury market is $10^13, it will have no issue accommodating a few buy orders from the $10^9 club

Is it sound to organize your economy in a way where the mere luck of owning real estate will net you the same income as what a specialized professional has to work decades to earn?

I don’t know how people (not 4%) are surviving.

How would the housing market bubble bursting affect people in this same situation?

When I bought my first house in the early 2000s, mortgage rates were in the 6-7% range. I remember my parents had a 13% mortgage in the 80s. Its only in the last few decade or so that we've seen these 5% or lower rates. I think we just have to get used to it, and maybe the AirBnB crash will help at least lower the price of the house and make things more affordable..

I often feel like a lot of social policy is simple as long as people understand the tradeoffs and everyone is on the same page. Unfortunately that has not been the case.

Here's a graph of the Bank Rate of the Bank of England (the UK's central bank) going back to 1694: https://fred.stlouisfed.org/series/BOERUKM

So, depending on your time frame, the 70s and 80s were abnormally high, post-2008 was abnormally low, and 5%-ish is "normal". (I think, if you keep going back, 5% continues to be kind of normal, but I don't have the data in front of me.)

It could be a 100% interest rate, without also looking at the cost / income ratio it's meaningless.

1. People simply choose not to sell their houses; as most people who own one or more homes have that option, or

2. The 64% of people buy the homes selling for cheap, and resell for a profit

The real issue in the US is going to come down to how many people can continue to afford multiple homes which is where rising interest rates and inflation both come into play. Anyone that bought a second home using an ARM may be forced into paying much more than they thought, and rising interest rates are going to put additional pressure on people with investment properties as they may need more liquidity sooner than originally expected to cover routine expenses.

The London rental market is if anything completely overheating at the moment due to lack of supply.

Except those who feel that prices will go down further and don't want to be left holding the bag. It's a classic prisoner's dilemma.

> The 64% of people buy the homes selling for cheap, and resell for a profit

With the current interests rates, this is straight up magical thinking.

It’s not. The current mantra is that if prices go down, on a timescale of like 10-20 years they will eventually go back up. This is the way things have gone for at least the last century. AirBnB can go bankrupt tomorrow and wit will do exactly nothing to dispel this thought.

> With the current interests rates, this is straight up magical thinking.

Do you think that matters even the slightest bit? A nontrivial proportion of homeowners could afford to buy second homes outright at this point.

Speaking of fantasies, the bottom of the page spruiks the author's latest e-book, "The Asian Heroine Who Seduced Me".

For our first meeting she’d chosen to wear a plain black halter blouse that showed her figure and bare shoulders to good effect and a peasant-style skirt of multi-colored, mixed- texture fabrics. Her dark cascade of hair was pinned up in a chignon, revealing her graceful neck. Her smile revealed even white teeth. She had the glow of the well-off and an unself- conscious confidence. She was poised, slightly shy and visibly curious about me.

In other words, she was stunning.

And needless to say, out of my league. "

While I have no clue how the housing market is going to turn out, I'd point out that edge conditions control prices quite often. When demand is higher than supply prices can increase very quickly, and the converse is true also.

If you talk to a lot of older Americans, a non-trivial portion of whom are invested in the housing market, their faith in the continued growth of the housing sector is akin to their faith in God. They’d rather sell their kidney than their second homes at a loss.

You would have to do a lot to get them to believe that the housing market is over.

There is a natural phenomena that forces people to vacate their houses.

Besides, its not residential homes that are a ticking time bomb, its commercial properties... Office workers are not going back to the office.

I am not seeing this. Major companies are forcing the issue, and employee can pound their refusal all they want but at the end of the day I think we not going to see a normal fully remote work force.

At best you are going to see a hybrid where you get 2 or 3 days a week of WFH, and the balance in the office.

Further from personal experience I somewhat agree with the management because I have seen LOTS of abuse of WFH from employees.

5/7 of the days, relocating an entire city worth of knowledge workers across town to a computer screen is fairly nonsensical.

You force everyone to live within a radius of economic hubs if they want job mobility, or you have to be comfortable relocating your family every N years for upward mobility in your career (or take the career hit, wait for internal promotions, and risk the company folding).

It’s socially not great. It’s economically not great. It’s environmentally not great. Working from the office is just all around not great.

Speaking personally, I live in a good community, with a good quality of life, a good school district, I can afford a good home here, and I can provide for my family. I’ve setup roots and intend to raise my kids to adulthood in this house.

I’d be surprised if anyone could afford a competitive package that would convince me to relocate my family, pulling my kids out of school, selling my home, and paying the toll of a daily commute.

The rest of my career is remote. Companies can do hybrid. They can return to office. They can do whatever they want. Unless they support full remote, I’m not part of their talent pool.

I know many people who think this way. And that number is growing.

From my own team, if I had to guess, the actual number of productive hours are similar.

Granted, I think it probably varies dramatically by company / team, and I get the impression that some places take WFH much less seriously than we do (as in, not goofing off).

isn't that the point?

force these to be rented in med to long term, or at least 1 year leases, so to open up the housing market for people who want to, like, live somewhere.

In NYC, another sign of STVR buildings are lockboxes chained to metal railings outside.

Starting tomorrow (September 5) such rentals are supposed to follow very strict new rules introduced by the Adams administration including hosts required to live in the same unit and reservation caps of no more than 2 people. Whole apartment rentals are banned unless the term is longer than 30 days.

https://www.thecity.nyc/2023/8/15/23832212/how-new-airbnb-re...

Maybe as a correlation, but these lockboxes are used for everything in NYC, dogwalkers, nanny’s, house cleaners, apartment viewings, etc.

Whether this leads to the "bubble popping" scenario described in the parent article remains to be seen.

Talk is cheap. Show me the maths. NYC has a vacancy rate of ~3%. That's the lowest in the country.

Maybe they're just not home?

The mental gymnastics folks go through to say "this behavior is ok if people I like do it, but it's wrong when those other gross people do it" always amuses me.

1. https://economictimes.indiatimes.com/tech/ites/infosys-ceo-s...

If you’re a large-scale real estate corp, the houses are just income earners and as long as the income is greater than the n expenses, you don’t give a rats ass who lives there.

This is fundamentally untrue, there is nothing "artificial" whatsoever.

AirBNB allows a city to host a larger number of tourists than hotels alone can provide, which stimulates the local economy with lots of spending etc. This is not "artificial", it's real local economic growth.

The scarcity of housing is then not caused by AirBNB -- it's caused by not constructing enough housing.

It doesn't matter whether demand for new housing comes from tourism or people moving to the city to reside. Demand is demand, and tourism is not "artificial". Nobody calls people moving to the city for work an "artificial" cause of scarcity, and neither is tourism.

The solution is to build more housing. Period.

I live in a tourist city - there's no shortage of hotel rooms. As tourists flood into livable dwellings, hotel vacancy rates have skyrocketed, and rents for the locals are skyrocketing as well.

Usually tourist cities don't have a hard time building new hotels. Building new housing can be tough. Hotel taxes are popular with the locals for obvious reasons. Property taxes aren't. NINBYs don't like residential density either.

For better or for worse, the only way out of this is through regulation.

How do you know?

It's not going to show up as hotels always 100% full.

If there was demand from 10,000 tourists, and there were 7,000 hotel rooms and 7,000 AirBNB properties, then you could have 5,000 (71%) of hotel rooms occupied and 5,000 (71%) of AirBNB properties occupied and you'd think there was no shortage of hotel rooms.

But there'd be no shortage of hotel rooms only because of AirBNB. The reality is that there'd be demand from 10,000 tourists and only 7,000 hotel rooms.

> Usually tourist cities don't have a hard time building new hotels. Building new housing can be tough.

Well tough on them. Lots of things are tough. I have no sympathy -- new housing should be built, end of story. It's not sending a man to a moon, it's just regular old governance.

It's very clear that many tourists want to stay in AirBNB's. This is a valid consumer preference to stay somewhere that feels more like a home, in a place that feels like a neighborhood instead of a busy downtown, with a normal amount of space rather than a cramped hotel room, and at less cost. It seems silly to say that's a bad thing.

But in any case no -- I'm talking primarily about the fact that tourists spend more on restaurants and attractions and shopping than locals. While I'm assuming that landlords just remain landlords.

Or if you're ambitious you borrow money against the house to renovate it and build it larger. Slack off at an easy job and you have energy to do renovations in the evening.

Every 10 dollars borrowed to do renovations becomes at least 20 dollars in increased home value when the renovations are finished, and as a bonus you get to live in the newly renovated house. You don't need to sell, instead take out another loan against your now more valuable house - the bank is eager to help. It's called a "real estate career".

Compare that to working for a living as your "career": Every 10 dollars of productivity you put in for your boss turns to 7 dollars in wages and after taxes you have 4 dollars. Not to mention the taxes and tributes as a small business owner or independent.

Which is the smart move? Which is the fool's move?

If you talk to everyday people, what is their dream? What would they like to achieve? Will they say they want to invent something? Create a huge business? Become best in the world or at least in their region in some sport or hobby? Very few will answer this. Most will answer: "I want to own a bunch of condos and live on the rent". That is the dream.

For context, here's nominal rent vs. nominal income, both indexed to 1985.

https://fred.stlouisfed.org/graph/fredgraph.png?g=18r0r

EDIT: Some criticisms of the charts the author uses:

1) The Case Schiller chart is in I guess "units"? The underlying data is an index to 2000, so saying it dropped '50' (going from 180% of 2000 to 130% of 2000) is for the most part meaningless. The farther you get from the year 2000, the bigger the numbers will look.

2) The investor purchases thing is just a noisy first derivative of the interest rate chart. (https://fred.stlouisfed.org/graph/fredgraph.png?g=18r18)

3) Population doesn't occupy houses, households do and those have grown faster than housing units. (https://fred.stlouisfed.org/graph/fredgraph.png?g=18r1T)

4) See above

5) There's a lot of complex policy debate about whether or not we are in secular demand crisis, but the MBS chart is all about lowering interest rates to increase demand. I agree that has unintended consequences, but the author seems to forget that builders pay interest rates too.

It's hard to argue with this ironclad circular logic.

I have yet to hear a convincing argument beyond "people will just stop selling their homes, forever," which is obvious nonsense. Once the adjustable-rate mortgages reset in a year-or-five, many, many folks will be forced to sell. Prices only come down when people are forced to sell at a loss.

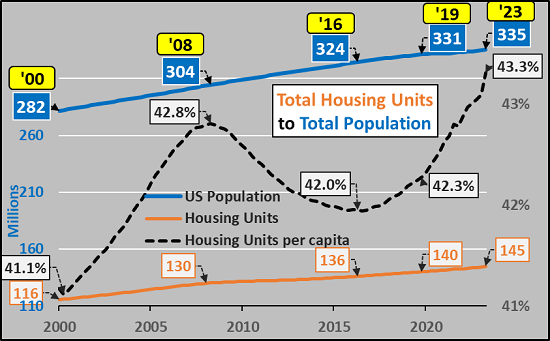

Specifically, as I write this, the OP states that the number of housing units per capita in the US is at an all-time high, per this plot (unless the OP changes it):

https://www.oftwominds.com/photos2023/housing-per-capita8-23...

Federal data shows otherwise. Here's the actual number of housing units divided by number of persons in the US:

https://fred.stlouisfed.org/graph/?g=18r64

Otherwise, I'm reluctant to call the US housing market a "bubble," because I haven't seen the classic signs of financial mania.

I don't know where this guy gets data but I don't think the availability is that far off from the peak. https://twitter.com/Econimica/status/1698596620022186428

You're talking less than 2 percentage points with the fed estimate anyway right?

This is going to create some other problems if the housing bubble does burst. The city has kept increasing the budget year over year.

They are banking on these huge valuations to fund all sorts of spending.

At the budget meeting, elderly people were speaking up on how they cannot afford the tax increase.

Property taxes are the only taxes that, by definition, the owner of the property can afford. The elderly people only mean that they "can't afford" their property taxes without changing their lifestyle in any way. To be fair to them, it's certainly challenging and uncomfortable, however, this is a consequence of their own making. None of them were complaining during the 30 years of their property values were going up as supply became more and more stifled.

investors should not be buying housing stock.

Do you have a job? Or did you forget about the 2008 wreck that took everything else down with it?

Even if that caused some _local_ downward pressure on house prices, why would that affect the demand for short lets? It might reduce the supply, so local room rates would go up. The remaining owners would have a lower-valued asset producing higher returns - a better return on a percentage basis, and in cash.

Few people holding cash-generating property will be pushed into selling by a dip; lots of them will have held through 2007-14. Property value as investment is (still) a bit of a religion here.

Councils and national regs have far more potential to dent Airbnb numbers (e.g. I'd guess we'll see sales tax added on nationally by the next government). But I don't see the political will anywhere yet, even in places like Edinburgh and London that have unusual regulation.

Some data here: https://www.housingwire.com/articles/datadigest-inventory-an...

"At stake is potentially millions of dollars in lost revenue for Airbnb in one of its biggest markets. Some 7,500 units don’t meet the requirements to apply for a license, according to market analytics firm AirDNA, and so will likely eventually disappear from the platform. More than half of those listings are frequently rented and account for about 40% of Airbnb’s income in New York City, according to AirDNA. In a lawsuit against the city over the rules, Airbnb said it earned $85 million in net revenue in 2022 in the Big Apple, which is about 1% of its total.

New York has been sparring with Airbnb for years over rules that prohibit rentals in most apartments for fewer than 30 days without a tenant present. AirDNA estimates that only 9,500 of Airbnb’s 23,000 listings are legal."

Will that few units (out of a city of 8.5M) coming back online really pop the housing bubble?

Popular Tourist Destinations tend to be places that people do not just travel but move to.

> Here's how we can tell if a speculative bubble is a bubble: everyone says it isn't a bubble

What an incredible sentence. Is a speculative bubble a kind of bubble? But then there's no need to tell whether such a speculative bubble is in fact a bubble. Anyway, we can tell if everyone says it isn't a bubble. Cars are a bubble. Lolipops are a bubble. Everyone says these things aren't bubbles, which means they must be.

So unlike bitcoin, housing cannot stay irrational and divorced from fundamentals forever. Real people need to use real paychecks and actual local credit unions need to look at those purchases and see a safe bet.

If that system stays out of whack for too long, everything collapses, the banks’ business model, the housing market’s prices, the ruling party’s majority, rule of law as the people resort to squatting and the capitalist system that failed in the simple task of keeping people out of the rain and cold.

Ive been there I tried that

Now a days I a bring a tent cuz I love waking up on a beach or on a pastureland with cows on the country side in the morning. You can also rent a cheap combi car and use it as a tent o vacation and go anywhere.

http://webcache.googleusercontent.com/search?q=cache%3Ahttps...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}