The pound dropped in value a few days ago, but the price has recovered since then.

The media chooses to focus on the drop rather than the recovery, because the drop coincided with a government announcement of some pro-growth economic policies that mainstream pundits disagree with.

If you speak to people in the U.K. many would agree that paying less tax is a positive thing, especially during a global cost of living crisis. But some people on the Left are angry that the wealthiest are also getting tax cuts.

What a lot of those people don’t realise is that the wealthiest 1% are paying 28% of income tax receipts - and this percentage has increased over the last decade.

In my opinion, I’m glad to see government reduce the tax burden on productive workers, as this stifled well-paying jobs, growth and investment.

I speak from personal experience. Due to the insidious tax policy of withdrawing the personal allowance when income reaches £100K, there is a marginal tax rate of over 60% at that income level. For that reason I chose to quit my job as a software team manager in an investment bank and instead went to work as a developer in a startup.

I decided there’s no point in working long hours in a responsible job helping other people advance their careers if I keep less than 40p of every pound I earn at that point. I may as well do less responsible work that I enjoy instead.

> I decided there’s no point in working long hours in a responsible job helping other people advance their careers if I keep less than 40p of every pound I earn at that point. I may as well do less responsible work that I enjoy instead.

This is an extremely funny takeaway in that anyone who doesn't agree with your ideological position is likely to see this as the tax working as intended.

Many people on the left see tax as an appropriate punishment for wealth.

In their worldview, wealthy people are demonised and dehumanised. The left are convinced that wealthy people are parasitic on society.

This leftwing ideology seems peculiar to me, having seen the data on who's funding public services, and who's benefiting from public services.

The issue is that most of the economy relies on people (including the lower classes) spending, which they aren't going to do if they already spent all their money on rent/bills. This in turn means businesses may go underwater if they aren't getting enough customers to stay afloat and operate profitably, leading to losses of jobs and less business for the companies that serve those businesses, and so on and so forth in a cascading failure. So even if you are selfish and say "fuck the poor", it's a bad idea because your ability to stay rich relies on there being "poor" people who spend their money at your establishment. Not to mention that with extreme poverty comes crime, something that ultimately costs all of us money.

It's like "tricke-down economics", except it trickles up and unlike the former, this one actually does happen for real and we're already seeing the effects of it.

I say this as someone who otherwise is in favour of tax cuts and sees taxation as theft, but that's a discussion for another day. But if you're going to cut taxes to help with cost of living and can't cut them all, then focus your efforts where it actually helps. The ones who will actually see a non-trivial increase in their income due to this cut are those who already didn't need any help.

I wouldn't say that it's just "some people on the left" - I dont want to place myself on either side of the fence but sky news are doing interviews with cross sections of Conservative / Labor / Swing voters and most of them think that this is Truss's fault.

You are correct that this has coincided with the dollar making gains against most other currencies, and the effects of the mini-budget may be difficult to dis-entangle from that, but from the people I've seen interviewed, most people agree that the mini-budget has at least made things worse for the pound. It's worth pointing out that the pound has fallen significantly against the euro too[0].

[0] - XE dotcom

Without any information on how wealth inequality has increased, and the 1% have more income and assets now than they did last decade, this is misleading at best. If the top 1% are paying more taxes but are also making more money, this hardly seems unfair.

It’s fair enough if you want to work at the startup but this seems like a strange rationalisation. I agree that the 60% marginal rate from the personal allowance reduction is kinda silly.

It doesn't appear recovered to me.

We're trying to boost the economy by cutting taxes on the group of people who are most likely just to stuff the extra money into investments rather than spending it? Great idea.

Also, this isn't just the left, it's practically anyone with a brain. Any conservatives from David Cameron's administration (not far right ideologues) are horrified by this, as are most of the current MP's who overwhelmingly wanted Rishi Sunak, who is also horrified by this...

I always viewed it as a cynical way to weaken labour.

> "policies that mainstream pundits disagree with"

That the Bank of England have had to scramble to compensate for by bringing back QE in a limited form, that previous governers of the BoE have spoken out against, that the IMF has spoken out against, that previous heads of the US treasury have spoken against, that conservative peers and MPs have spoken against, that the markets responded to by having a fire sale?

Those are a few mainstream pundits? LOL.

> If you speak to people in the U.K. many would agree that paying less tax is a positive thing, especially during a global cost of living crisis

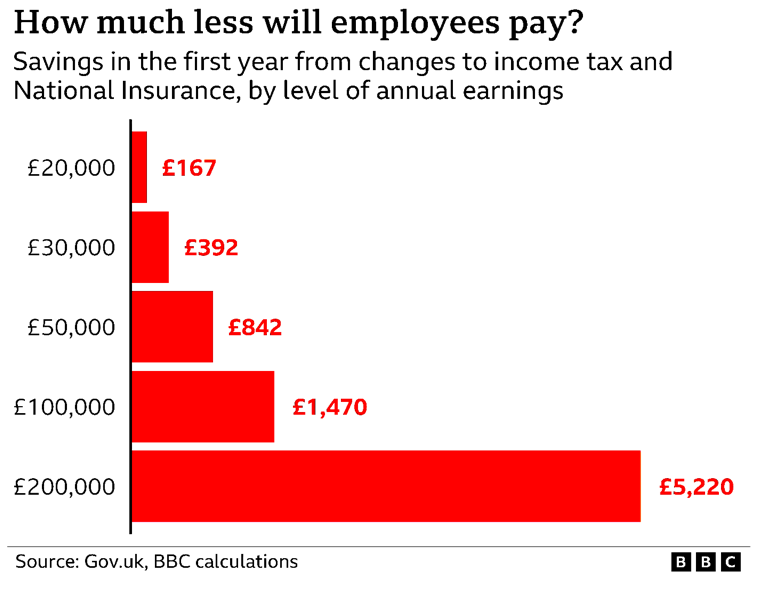

Very few of those people would be paying less tax under these plans, as the major reduction is for people earning over 150k per annum - and those are the people already best placed to weather the cost of living crisis.

It's not that the wealthiest are also getting tax cuts, it's that virtually nobody else is.

I'm a high earner and I like money, but this is some self-interested bull**** right here

And the IMF has consistently got it wrong about the UK economy. In the past it has actually made public apologies for doing so (IMF head: "do I have to go on my knees?" regarding incorrect warnings on UK economy): https://www.telegraph.co.uk/news/politics/10884632/Do-I-have...

We have to be careful to avoid the Argument from Authority fallacy, using the IMF and BoE reaction to judge government policy. https://en.wikipedia.org/wiki/Argument_from_authority

> It's not that the wealthiest are also getting tax cuts, it's that virtually nobody else is.

When the most productive members of society got landed with a 45% tax rate in 2013, it was higher than many G7 nations, and there's no evidence to suggest it actually increased revenue. Have you heard of the Laffer Curve?

The trickle-down maths looks "optimistic". Cutting £45B means that the economy needs to grow by £112.5B for the top rate 40% tax rate take to come out even. That is GDP growth of 4.5%. I.e. far in excess of what the economy has been capable of ever since 1997.

Talking of further tax cuts just pushes the assumed GDP growth further into fantasy land.

Also, despite 10% inflation they’ve frozen the tax bands, so all workers earning above about £12k will have more of their income pulled into higher tax bands.

So they’re left with that artificially high rate which blocks progression, and most workers up to about £150k will pay more.

Can't you just put that in your pension to avoid that effective 60% rate?

> no point in working long hours in a responsible job helping other people advance their careers if I keep less than 40p of every pound I earn at that point

I think the way the UK calculates tax at that level is a stupid way of setting it up, but "only" taking 40% of the 100k to 125k is hardly terrible. If you're in that range, you're incredibly well paid for the UK (or pretty much anywhere in the world).

I would personally like to pay more tax if it meant decent public services instead of people dying waiting for ambulances.

The affect of removing that doesn't seem to be that major, with the figures [1] appearing to work out at almost 1.5% less tax for those on £100k, and a little over 2.5% less tax for those on £200k -- hardly a huge decrease in the tax burden for those people.

[1]: https://blogsmedia.lse.ac.uk/blogs.dir/8/files/2022/09/28sep...

Also, when you are that income level, there are a number of tax benefits you can enjoy - for example the first £40k you put into your pension is before tax - so it effectively reduces your salary (for tax purposes) by £40k. SO if you are doing the sensible thing and putting money into a pension, the threshold you talk of is effectively at a £140k salary.

It also reduces your actual salary by £40k, not just for tax purposes, if you'll never end up using your full pension. Either because you've died before doing so, or because the pension fund can't pay you out (fully) since it is increasingly underfunded due to a rapidly aging society.

Answer this honestly for yourself: if you are fairly young, say 25-35, what are the odds you'll see more money in your lifespan from £40k put into a pension now that may or may not be fully available after retirement, versus £40k minus tax invested into an index fund and accessible/reroutable whenever?

It's not my "privilege" to earn at that level. I was born into an average economic background. I worked really hard at school and university, and then over a period of seventeen years, I worked really hard in responsible jobs.

If all people from average backgrounds took the attitude that only "privileged" people get good careers, then unfortunately it would be a self-fulfilling prophecy. Luckily there are plenty of aspirational people in the UK looking to better their family's situation by advancing their careers.

The obvious incoherency of this then led to the markets losing confidence in the UK economy, crashing the value of the pound, which in turn makes the planned UK debt funded tax cut plan even more expensive than it already needed to, leading to even more loss of confidence.

We are now in cascading crisis, from which there are no good option, only worse and terrible ones.

The thing I am confused about is why this happened at the announcement. The big measures had already been announced, an energy price cap (£60bn or more depending on wholesale gas costs), and reversal of planned tax increases in National Insurance and Corporation tax (about £40bn). The additional unannounced tax cuts were small (for instance the cut in top rate tax was £2bn). So it seems that most of the drop should have happened before.

Apparently the PM wanted the announcement to feel radical to distance her from the previous government, so maybe the markets were responding to the feeling of the announcement, and the implication of future radical ideological action, as much as the numbers.

I'm far from an expert, but to be totally honest I think most people didn't really expect it to happen this way. The media were all talking about how it's not possible and no one knew where the funding would come from. Everyone was mostly expecting it to not happen to be quite different and more complex.

It turns out we overestimated both the PM and the Chancellor.

My understand is that it’s exactly this. So much of the markets comes down to vaguely defined “confidence” and the new leadership simply isn’t inspiring faith from those in charge.

Isn't it more the conflicting policies (BoE and gov) in theory and the perception of them not being in the same page?

This avoidance of accountability is a repeated pattern in British politics recently. Turns out you can bend our political system that way, but the global markets really don't appreciate that behaviour.

One economist said that Britain is now paying the Moron Risk Premium.

Here's potentially a better description: The new government came in and announced a series of policies that made it immediately clear to markets that inflation was not being taken seriously in the UK. This lead to a drastic, and I mean historically drastic, sell off on the long end of their bond market. Basically all capital markets in the UK were on the brink of freezing and probably shortly thereafter this would have become systemic.

This would have basically set the timer started on the UK being maybe a few weeks off from a humanitarian crisis. (if you think this is hyperbole understand that the entire energy storage capacity of UK is about 1% of their yearly use meaning capital financed energy flows are constantly necessary to keep the system running, the food situation is not that severe but still requires flows)

After all of this occurred, the BOE came in did the thing that they had zero other choice but to do which was to inject liquidity back into that segment of the bond market. I think they would be the first to tell you that this policy is a disaster. They had absolutely no choice.

If any of our US friends were wondering what that is in your currency, it's about 100 billion dollars (following our new PM's economic "experiments").

Sure it might be disastrous for Truss, or Government, or The Conservative party. But for the UK as a whole it must be the reasonable way out?

Have you ever seen authority figures backing off? When questioned or face backlash, they only double down. In fact, that's what happened - the official word is "this is the right way", and "the government is not responsible for market movements", "it sends the wrong message to tax windfall profits", "The poor can't pay bills? That's fine, we'll cut tax for the rich - that'll fix it".

#KamiKwasi, as Twitter called it, will continue.

Not to say the tax cut is not a terrible idea - it’s absolute stupidity.

https://www.cnbc.com/2022/09/30/ron-insana-something-big-cou...

Money comes in money goes out, the difference is made up with debt. Tweaking either the income or the outgoing knobs impacts the debt required. So a tax cut requires extra debt to make up the difference.

The UK central bank, the BoE, is forced to take measures to counteract what Truss and her government are doing !

The market is also strongly reacting against Truss by selling the pound.

The tax breaks though, were totally an own goal.

Reading https://www.bruegel.org/dataset/national-policies-shield-con..., the UK allocates about double of what France, Italy and Germany allocate to it.

Secondly, all else being equal, lower taxes certainly would attract talent and business to the UK and overall make people better off. As a simple example, let us consider an extreme case where the UK has a 20% flat tax while maintaining macro/political stability, and that rate is expected to persist. For starters, there will be a huge move in tech from SF and NY to the UK. It will become a very desirable destination for top talent; startups and unicorns will follow. With clever tax incentives, it would not be just London either, but cities all around the country. That influx of talent and capital would benefit the middle class and the poor too. The one bottleneck, as is usually the case, would be housing - if that is also resolved (say, making it really easy to build in/near currently depressing-looking cities), there could be a real boom to the UK economy.

As things are going now, this is unlikely to play out in the UK, unfortunately.

Source: https://www.gov.uk/government/statistics/percentile-points-f...

> but Truss’ announcement came in the middle of the worst bear market in bonds for well over a decade

Yes, and she chose to do that. It was amazingly irresponsible. The market response was entirely predictable.

I'm an economist and this is wrong. I usually see this line on on Reddit and not from any journal.

Rishi Sunak was a better choice in every category, but had two problems:

1. he is not "white"

2. he is not anti-Russian enough

EDIT: By "elected" I meant "elected by her own party".

The former PM resigned due to scandal and Truss is a drop in replacement "elected" by a tiny tiny number of elites isolated from the public at large.

Also, the most popular candidate with the Conservative membership was Kemi Badenoch, who is black, but far more radical than Rishi Sunak, who was forced to defend Treasury orthodoxy.

I’m not convinced it has much to do with race.

The latter course of action wouldn't have been wildly popular with voters (even those outside the 100k party members that made the selection who are a lot more impressed by Thatcherite postures than the average person), but it wouldn't have sparked the present response from forex and financial markets.

I though markets reacted negatively to socialist governments getting into power, not the opposite.

Normally left wing governments are punished because they increase spending without increasing tax revenue - causing unsustainable debt. The UK has done the right wing equivalent - they decreased tax revenue without decreasing spending - causing unsustainable debt.

Truss's administration is giving tax cuts to the wealthy and paying for it by borrowing. The markets know that trickle-down economics is nonsense and these tax cuts won't boost UK's economy enough to cover the enormous amount of debt required to pay for them.

As an investor you always want your investments to yield more than the rate of inflation and when government policy increases inflationary pressures by fuelling growth the market will demand higher interest rates. Of course there is also uncertainty about how the government will pay for the debt which is increasing the risk premium.

It's just dumb fiscal policy to boost growth at a time when central bankers are trying to do the opposite. It would probably work great during a deflationary period. Its just that's not where we are right now.

Usually, the right-wing, and the "markets", agree on what is good for the economy. It is quite unique to see the "markets" disagree so strongly with "the right".

And it is also worth noting that it is quite rare to see left people use the view of Wall Street as an argument ! I remember many cases in Europe where socialists governement almost used it as an electoral argument that they would ignore "the markets" (or rating agencies) and not dictated their policy by what they said

Either there is no realistic plan or the ministers involved have been too incompetent to explain it. Neither explanation inspires confidence.

By fuelling growth in a period of high inflation with debt you basically add to the existing inflationary pressures and increase risk.

As an investor you want your investment to at least yield more than inflation so this is one reason why the market is demanding a higher interest rate (the market now excepts UK inflation could run hotter), but they're also worried about the risk of extra borrowing so are also demanding a higher risk premium because of the uncertainty of their investment.

Also, I'd argue this isn't really a "right-wing" fiscal policy. Cutting taxes might be "right-wing" but borrowing to do so certainly isn't something that's universally popular with those on the right. Most on the right probably want tax cuts to be funded by spending cuts.

It has solved this problem over the years by borrowing and becoming a haven for investment to cover up the shortfall.

Now we have a bat shit government that says we need to lower taxes and borrow a boat load of money to tide over the energy crisis. The markets don’t see how this borrowing will improve the UKs ability to earn more dollars (or the govt to raise more taxes).

In essence the market realizes that the UK is going to repay its loans by printing money.

Hence the pound tanks in anticipation of it. One way to stop this is to raise interest rates and pull pounds out of circulation but the government is terrified of popping the real estate bubble.

TL;DR - The pound will keep falling and the UK will lose its social services but don’t take this as investment advice.

I'm pretty sure i'm being naive here but... why?

House ownership has become a huge problem for recent generations in the UK, I still haven't engaged with the market because it's so hard to get a foot in the door unless you have masses of disposable income. Popping the bubble would help a lot of people in the UK to begin a more healthy long term financial life (i.e compared to pouring a huge chunk of your income into the pockets of landlords instead of a house you end up owning).

Is it that at a market scale there would be repercussions outweighing the obvious benefits to citizens? Or are they just protecting the rich who want to maintain the value of their "assets".

> One important effect has been on the interests and aspirations of the electorate: the last thirty years have witnessed an expansion in the number of voters who have a vested interest in the buoyancy of the housing market, and a marked decline in the constituency of voters with an interest in social housing

> This has triggered a shift in political attitudes on issues of housing and resulted in a much greater focus on meeting homeowners’ aspirations. Overall these factors represent a profound shift in the way that land and property has been perceived in British society.

> Whereas 100 years ago houses were mostly regarded as simply somewhere to live, today homeownership is promoted as an investment opportunity which offers long-term financial security in the face of stagnating wages, dwindling pensions and reduced state welfare provision. To politicians and much of the general public alike, houses are no longer perceived as universal consumption goods but rather as vehicles for accumulating wealth.

> Homeownership has become perceived by many as ‘the essential step to obtain membership of an expanding middle class for whom housing equity was pivotal in a broader lifestyle of credit based and housing equity fuelled consumption’ (Forrest et al., 1999). [...] underpinning this has been a deregulation and liberalisation of the financial sector and a rapid increase in income and wealth inequalities.

> This marks the final major shift in land’s economic significance, as high levels of owner-occupation, a deregulated housing finance system and growing inequalities have combined to create a system of ‘residential capitalism’ (Schwartz and Seabrooke, 2008). In turn, the political dominance of homeowners – both in national elections and in local planning decisions – has ensured that their interests have been protected and subsidised by government policy (Keohane and Broughton, 2013).

For the avoidance of doubt, I don't think this is a desirable or sustainable situation. I just thought it was helpful to expand on the contributing factors.

The government doesn’t get to decide this. Interest rates are set by the Bank of England and will rise as a result of the government’s decisions. So it’s more accurate to say that the government doesn’t care about popping the real estate bubble or is delusional about the effects of their policies.

High energy prices due to pound weakening against dollar = Bad

[1] - https://lookingglasseducation.com/whats-a-debt-spiral-and-is...

It’s not the money that’s the issue - that’s an abstract, invented thing. The limits are inflation, natural resources and available labour.

There's a good article in the Financial Times that explains the mechanics behind it ("LDI: the better mousetrap that almost broke the UK"): https://www.ft.com/content/f4a728a5-0179-48bd-b292-f48e30f86... (archive link: https://archive.ph/vRrGk)

tl;dr from the article:

"Well, the cruel irony is that pensions needed collateral for margin calls on leveraged trades hedging against big moves in . . . UK government bond yields.

So pensions sold bonds (among other things) to raise that cash, pushing yields up, making hedging trades even more expensive, and requiring even more collateral.

If the BoE hadn’t stepped in to arrest the declines, pensions may have defaulted on those contracts, which would have been very bad. That isn’t the same thing as going bust – it’s not like all the investments disappear overnight – but it does risk tying up the pension in a knotty legal fight over settling the default."

When it became clear that having enormous debt inevitably causes instability when people doubt the government's ability to pay this back, pension funds became responsible for not just funding the government, but also guaranteeing the ability of the government to loan more money. This requires leveraging their investment, and THAT is what's causing the crash here, that leverage. They've effectively guaranteed N times the government_debt, and that N is what became "big". That guarantee doesn't help pension funds, it keeps government debt payments low. The market is saying they don't want to lend to this government, and the government (not the PM, the rules for pension funds that already exist) is trying to force the availability of cheap debt. Of course, not using their own money or budget, but using pension money of ordinary people. This became out to be so incredibly expensive that even pension funds were in danger of not being able to pay for it, so the BoE lowered government funding costs using money printing, against their policy.

Pensions the way they were introduced after WW2 in the majority of places are utterly unsustainable, and the UK is no exception. If you calculate what a person needs to have an acceptable pension at the yields we've seen, you get to about a million pounds per person (2% drawdown, 2% investment yield, for 30 years, giving a person 25k GBP per year after tax = roughly a million. And that's generous, assuming interest rates go up and stay up, on average, above 4% without dropping average stock market returns below 4%, and with dropping inflation to ZERO 0%, because at 2% over 30 years, it's of course more, if you want the standard "parity" investment to work out). Pension funds actually have about 50k per person, not even 2 years worth of pension.

Pension funds are going to crash, obviously, and what Truss and Kwarteng are trying isn't the cause of that. In fact, huge inflation ought to delay the point these funds will crash. It's a matter of when, not if, and not a question "who is in office when it happens". I actually think their odds of preventing a pension fund collapse during their term are pretty good.

The government is back to the 1920s: they've found a way to force the government budget to be money printed by threatening pensioners livelihoods, and thereby can now effectively spend infinite money. This will of course cause massive inflation, but it will as was demonstrated, save pension funds. It won't, of course, help pensioners. They'll lose big in effective purchasing power. And that is exactly the point of this policy.

I have yet to see an exact model that shows this. Obviously it could not be one to one because of residential/commercial credit based on a fractional reserve system.

I really hoped the new leader would be the one with an economics background instead of the friendly optimist. Navigating out of brexit and covid is difficult and the leader sets the tone for how we're going to approach it.

The market deciding the UK is financially unsound seems a legitimate response to our strategy of copy the wise ostrich. Hopefully the people who chose Truss have made enough of a loss this week to reconsider their priorities.

Except Kwarteng's former boss Crispin Odey is making a killing shorting the pound. https://www.independent.co.uk/news/uk/politics/tory-donor-pr...

It's hard to make more from shorting the pound than the loss across your entire estate from sterling crashing though, unless it's now common for wealthy conservatives to hold most of their assets in dollars instead of UK real estate.

The FTSE250 is down 7% over 5 days.

If your fiscal plan doesn't make sense market lenders may not be willing to lend to you or will at least expect a higher interest rate to compensate for their risks.

The Conservative party in the UK has just elected a new PM who has announced a fiscal plan which doesn't add up - tax cuts financed with borrowing.

Worse still the PM is doing this in an effort to boost growth which only adds to current inflationary pressures at a time where inflation is far too high.

Given this the market now believes the central bank will need to be much more aggressive in their fight against inflation and raise their base rate much higher.

In addition to this the market is also sceptical of the governments fiscal policy and is demanding a higher risk-premium to lend money.

The result is sky rocketing borrowing costs for UK consumers, businesses and the UK government.

Pension funds are one of the largest holders of government bonds as they're typically seen as very safe investments (especially within developed markets).

But of course every investment still has risks and when those risks are underestimated it can leave a lot of investors on the wrong side of the trade very quickly.

As large holders of government bonds many pension funds found themselves in this position and my understanding is that some have been on the verge of blowing up in recent days.

Obviously were pension funds to blow up on mass this would have all kinds of negative knock-on effects for the economy.

It would also mean many of these funds would become forced sellers of bonds and this forced selling would have added even more volatility and instability to an already volatile market.

Basically the UK was at risk of at risk of a GFC style blow-up so to restore stability the BoE was forced to step in yesterday to buy bonds that no one in the market wants to own right now.

Interestingly today the PM is doubling down on her fiscal policy. But then she has some fairly controversial economic views, including the belief that higher interest rates is a good thing.

In my opinion she's too naive and ideologically driven to understand what she's doing. At the end of the day the BoE can't make a broken fiscal policy work, they can only buy time.

If the government doesn't reverse course the UK economy is probably going to implode, but as I say we have a PM so ideologically driven that she may actually see this as a good thing - it's just free-market capitalism cleaning out the weak-hands, etc.

Although it's probably electoral suicide my guess is the Conservative party will need to step in at some point and force her to back down in one way or another. If they don't it's hard to see the public will forgive them for this anytime soon. Especially considering many vote for the Conservative party because they're seen as the party of fiscal responsibility.

Either way as a mortgage holder who's probably going to default on their mortgage due to all of this I don't expect anyone to step in and help me =) This is my mistake, not the governments. And I'm just a pleb with a family, not a pension fund.

As the Fed raises rates in the US it makes the dollar a more attractive place to put money. This devalues other currencies against the dollar.

Because the dollar is the reserve currency a lot of stuff countries like the UK imports is denominated in dollars (oil, food, etc). This means the US actually increases inflation pressures for other countries when they raise their domestic interest rates.

This forces other central banks to raise interest rates in line with the US simply to protect their currencies from the inflationary effects of currency devaluation.

Unfortunately right now Europe can't really afford to do this with an ongoing energy crisis, but we have no choice. The US is literally whacking their allies around the head with the US dollar.

But then from the US perspective what choice do they have? The Fed already has little credibility and to allow inflation to run hot in the US to protect Europe from currency devaluation would be equally risky and unpopular.

We're in very tricky times. We've kicked the can down the road for so long that it's now catching up. We no longer have any good options left. It's all just trade-offs from here.

Many including myself did try to warn this was always the risk of such a reckless response to Covid, but I suppose it's too late for that now.

It's still hard to fully discuss the overreaction to Covid in many forums without getting shouted down for wanting to kill Grandma, but there are people out there who don't seem to fully grasp that actions taken to try and solve problems can have drastically negative consequences. You can't just spend money you don't have indefinitely without paying the piper and screwing yourself down the road.

Personally, I fear that the emotional reaction to Russia/Ukraine is turning the same way, perhaps with far more dangerous long-term consequences.

"...due to the almost £45 billion a year of tax cuts announced by the Chancellor today" https://ifs.org.uk/articles/mini-budget-response

2020 was record money printing, causing inflation, so Liz Truss set a plan to reform quantitative easing to try reduce inflation, and the markets reacted bad

The age old question, are banks to big to fail? What will happen to saving, mortgages, pensions etc... if you start restricting bailouts? Maybe some will just take their money to EU where they still have a cushion, in the always win casino

But no doubt reform is needed

In effect what is on offer in these auctions is a government promise to pay a certain amount of money at a set time in the future. Bidders say how much money they will pay now for that promise. For example maybe the government wants to pay £105 in 2050, and the auction just settled at £86 and I was a bidder, I pay £86 now, and I get a promise to pay £105 in 2050. The governments gets £86 now which it can spend, but needs to find £105 to pay me in 2050 (Hint: It will just issue more gilts).

Gilts are a bit more complicated because they have index linking and there's a whole coupon mechanism so you get a little bit of the money back periodically, but this gets the basic idea across.

The exchange rate stuff has a more immediate impact because it causes import prices to jump, but the gilt problem is actually what means you shouldn't ever do this. It's like using credit card debt to finance a fun ski holiday versus to buy a car so you can drive to work. One of these things is reasonable, albeit not ideal, the other is just throwing away money. Unfortunately it isn't Liz's money, it's the nation's money, increasingly it's the money of those least able to afford it.

Pension funds require new investors to pay off old investors - pensioners - until the pensioner dies, we have a word for that concept but it derails discussion.

Some large pension funds in the UK had borrowed against their investors capital, specifically for riskier speculation, which is necessary to guarantee the returns to the investors (pensioners).

The volatility in the currency and specifically UK government bonds (GILTs) caused a collateral call on the pensions, which would have first caused forced selling, a cascading pressure on the bonds and currency, and also eventually bankrupted the pension (which could honestly still happen).

In the longer-term, is it the slow accumulation of a thousand cuts?

-- Brexit

-- Stagnating physical output of UK industry (aside from finance + healthcare)?

-- Aging population

-- Expensive living costs + recent inflation

I don't know how much each of these factors has contributed, or if there are other important factors missing above. But for me, having lived there and seen the general situation, the question is, how will the UK renew itself as a country from a long century of gradual decline?

Came as a surprise, in a nonscheduled budget & was the opposite of what was expected.

That got the gilts (uk bonds) to drop, and that got the currency shocked as the gilts were force liquidated. I wouldn't read too much into the currency bit, as every other currency is down against the USD, including the euro, yen and aud.

However, if your currency is NOT the US dollar, then its a catastrophically bad idea.

In short: Truss and Kwarteng are intellectual lightweights whose economic ideas make for funny reading* but in reality are a recipe for disaster. Their line of delusional thinking can be traced directly to Brexit, when the UK lost their collective minds.

Interest rates are now expected to triple to 7% to cope with this fiscal event and as most UK home owners borrow money on revolving short term loans to buy houses many people are looking at a $1,000-$2,000 / month increase in interest payments and a 20% collapse in the value of property.

Most major businesses have gone into crisis mode (hiring freeze, paused expansion plans) which will have its own knock on consequences. If we're very very lucky it won't spread to other countries.

Typically these slogans seem to mean that a politically significant number of people are losing their jobs, but simultaneously used as cover to print money and give it to the wealthy. But I don't think that is what is meant right now in the UK.

They're quite obviously doing a smash-and-grab on the country for their remaining time in power.

>How not to run a country - Liz Truss’s new government may already be dead in the water

https://www.economist.com/leaders/2022/09/28/how-not-to-run-... (no paywall: https://archive.is/QWtQW)

The public after Boris went: "thank the gods that idiot's gone, nothing could be worse!"

The conservative party: "we really need to lose the next general election! We don't think Boris managed that."

Truss and Kwarteng holding hands: "hold our beers! LEEROY JEEENKINS!!"

This has been going on for a while, but even Johnson wasn't as directly controlled by this group. They took the opportunity to get rid of him and put Truss to the PM's position, making sure that she will do exactly as they tell her.

{kind=link}