This is where the value of all that liquidation preference kicks in. At some point it becomes in SoftBanks interest to push for lower valuation, as it means they get to wipe out all the people that came before.

Liking 20% ownership at 50bn doesnt mean you like 70% ownership at $8bn. The value of the company had significant future growth/hype component which required other investors to pour additional money in to keep up the growth, that is now gone.

------

Sure, but $20B valuation seems hard to achieve.

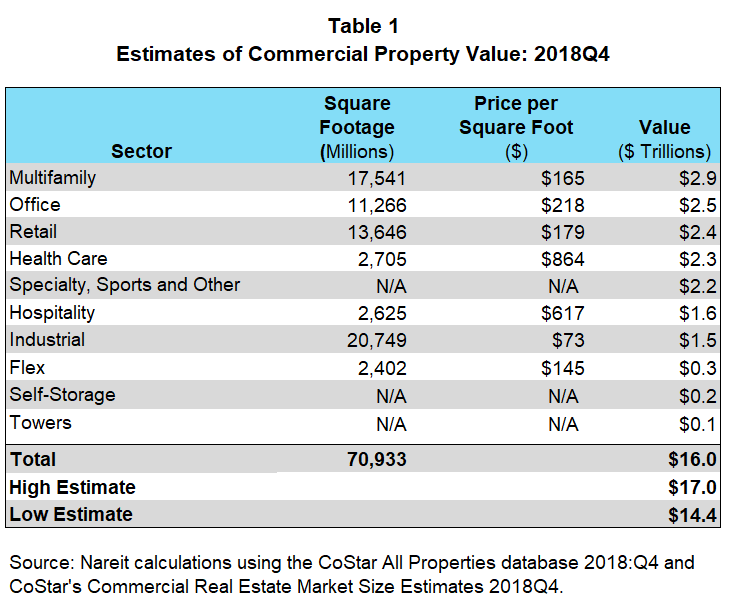

US commercial real estate market by revenue is ~$1.1T [0]

Office space by value is about 1/8th [1]

Regus gross margin is ~16% [2]

Real estate generally has good PE ratio but partly because they usually own the property [3], so let's be generous at 30x.

So if we value WeWorks as a normal real estate company AND weworks has %100 of US office real estate business we have a valuation of 1100 / 8 x 0.16 x 30 = $660B.

Now, weworks exists outside of the US, but the valuation you propose means they must have ~equivalent of all US office real estate.

[0]- https://www.ibisworld.com/industry-statistics/market-size/co...

[1] - https://www.reit.com/sites/default/files/chartjuly92019.png

[2] - http://www.annualreports.com/HostedData/AnnualReports/PDF/LS...

[3] - https://www.investopedia.com/ask/answers/052815/what-priceto...

Many of the best companies look like risky bets at the start.

SpaceX likewise is also in a somewhat murky financial position, although I suspect they will come out doing great in the future. My limited understanding is they are avoiding an IPO because their financials are not up to snuff.

AirBnB was heavily derisked before serious investors took notice - YC loves talking about them as an example because they had so much trouble raising a seed round before they skyrocketed into their A round shortly thereafter. Also I suspect AirBnB is actually going to IPO at a lower valuation than their last round, but I realize I am very much an outlier with that assessment.

I understand high risk high reward, but sometimes investors are just being dumb. I feel like you chose terrible examples to make your point. And since all of your examples are private companies it is impossible for us to analyze their finances.

{kind=link}