"MLR measures the share of health care premium dollars spent on medical benefits, as opposed to company expenses such as overhead or profits. For example, if an insurer collects $100,000 in premiums and spends $85,000 on medical care, the MLR is 85%. In general, the higher the MLR, the more value a policyholder receives for his or her premium dollar. The ACA requires an annual, minimum 80% MLR for individual and small group insurance plans, and an annual, minimum 85% MLR for large group plans." [1]

I mean, this is a constant joke in professional circles. If you are hourly billing and you can use your shitty talent to create something in 8 hours that your good talent would create in 1 - it's usually economically beneficial to have the worse employees do the work as it's more profitable overall. Up until the point where you lose the customer - but in this case that's not a concern.

Why? It seems that if premiums are rising relentlessly for one company that the insured will seek out other companies, and hence that one company will "lose the customer".

Or am I missing something?

Seriously, something is wrong with the whole setup. ACA does address some of it but it has jacked my premiums sky high. Single Payer is the answer in my estimation. The sooner we come to this and stop fiddling around trying to make people we shouldn't happy the better off we will be.

Some business (like insurance) have a fair bit of tail risk they need to take into account.

Some are seasonal (like a ski resort) and need to make sure the profits they make in their high season can carry them in the low season.

Some are cyclical (like furniture stores) where people buy one piece and don't buy anything else for years.

Grocery stores have consistent customers and can generally predict their income and expenses day-to-day for the foreseeable future.

The personal auto insurance combined ratio rose by 1.4 percentage points in 2015 to 97.3 percent for a group of 10 publicly traded insurers.

http://www.insurancejournal.com/magazines/features/2016/03/0...

When interest rates are higher car insurance runs > 100% loss ratio. They stay profitable by earning short term interest on premiums before paying out claims.

In a different insurance vertical fixing loss ratios at 80% would be called a cartel, and would put involved executives into prison for a good long time.

In healthcare the government forms the cartel, fixes the prices, gives money to poor to become consumers, and then fines everybody who won't become the consumer.

said Brer Rabbit. "Only please, Brer Fox, please don't throw me into the briar patch."

Second, a profit margin will take into account risk. So for the ski resort or the furniture store that includes the overhead of keeping the store open while you have no customers.

Third, if the risk is so insanely high why are these firms so consistently profitable? Shouldn't we expect to see them coming in and out of existence regularly? Restaurants are a truly high risk business venture, the majority fail to exist after the first year. Perhaps they have longer runways but it's rare to hear of an insurance firm shutting its doors. The large and consistent profit seen on their end of year reports belies the risk claim.

Sunlight is an amazing disinfectant and it is my hope that our government mandates every doctor and facility publish the total cost of every prescription and procedure they employ. We will collect that data and disinfect the high cost of health care.

[1] https://www.fisherbroyles.com/marketers-for-compounded-pain-...

By comparison, Bush's Medicare Part D prevented the Feds from even negotiating drug prices. Its author, Billy Tauzin, is now a Big Pharma lobbyist.

[1] http://www.factcheck.org/UploadedFiles/2015/02/kff-chart.png [2] http://data.worldbank.org/indicator/SH.XPD.PCAP?end=2014&loc...

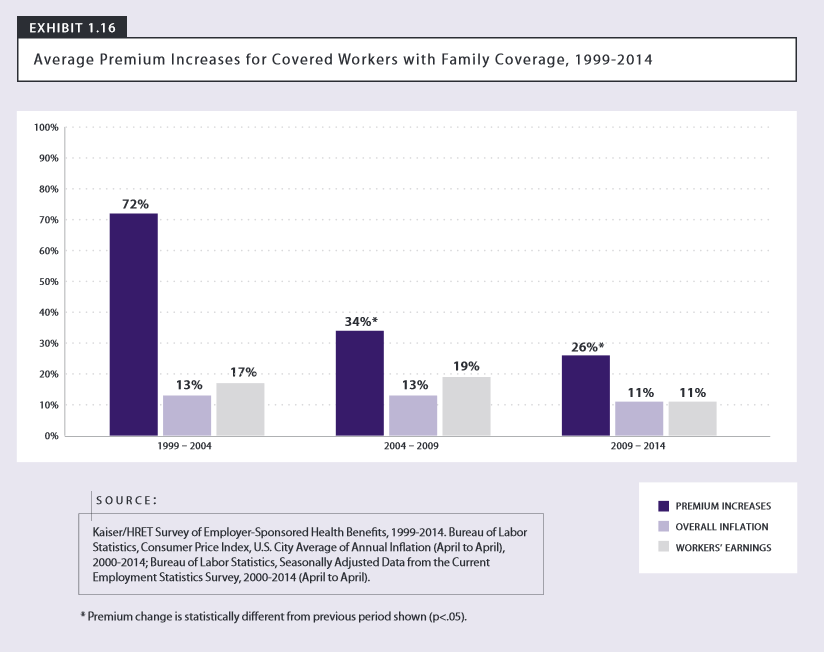

Before ACA, our premiums went up ~5% per year - 8% one year - every year was under 10%. Since ACA, I've seen increases of 25%, 20%, 20%, 25%, then 11% then 13%. This is in NC with Blue Cross - the numbers possibly were different elsewhere (was in Michigan before that but wasn't paying as much attention, unfortunately).

The price increases I was seeing seemed primarily in line with inflationary numbers pre-ACA; post-ACA they seem to have no correlation to inflation, and seem to have more to do with a much larger overall cost for the insurance company covering more people, no lifetime caps, more services covered, etc.

EDIT: On, that factcheck chart - that looks to be showing premium increases for employer-provided health insurance. Employers cutting back their contributions to the premium would account for much/most of those increases. Effectively, it doesn't say anything about the actual insurance premium increases, only what employer-covered workers were having to pay - in my view, that's a big difference.

http://blogs-images.forbes.com/theapothecary/files/2016/04/S...

It was the recession.

Unfortunately, I think it's percentage cap, not an absolute cap. So, if you're an insurer and want to increase profits by a dollar, you need to increase costs by a few dollars.

{kind=link}

{kind=link}